Valuation: what it is and how to value a SaaS company

By Tiago Costa · Updated on July 9, 2026

Definition

Valuation is the estimate of what a company is worth. In SaaS, the most common shortcut is a multiple on ARR.

- Valuation = ARR x market multiple.

- The multiple grows with growth, retention and efficiency.

- Post-money = pre-money + investment, and that sets the investor equity.

What valuation is

Valuation is the estimate of what a company is worth at a given moment. It is not a fixed price nor the book value of assets, but a market read of how much someone would pay today for a slice of the business, looking at the revenue it generates, the pace at which it grows and the odds it keeps growing.

In a SaaS, that estimate almost always revolves around recurring revenue. Because revenue repeats month after month, it is predictable, and predictability is exactly what gives the confidence to put a price on the company future. That is why a SaaS valuation is usually expressed as a multiple of ARR, rather than a multiple of profit, as happens in more mature sectors.

The ARR multiple: the SaaS shortcut

The most common shortcut to value a SaaS is to multiply ARR by a number, the so-called multiple. If a company has $10 million ARR and the market pays 6 times revenue, the implied valuation is $60 million. It is simple to calculate, easy to compare across companies, and the math investors do in their head in a first conversation.

- Valuation = ARR x multiple.

- The multiple is not fixed: it varies with the market cycle and with the quality of the business.

- The more predictable and efficient the growth, the higher the multiple the market will pay.

These multiples are not stable over time. In cycles of low rates and optimism they expand; in tightening cycles they compress. Firms like Bessemer track public SaaS multiples precisely because they act as a thermometer for the valuation of private companies, which trade at a discount to that public benchmark.

What drives the multiple

Two companies with the same ARR can be worth very different amounts, and the difference lives in the multiple. Three forces pull it up or down: growth, retention and efficiency.

- Growth: the faster ARR grows, the more future revenue the buyer is acquiring, and the more they pay for it.

- Retention: a base that does not churn sustains growth without relying only on new sales. According to SaaS Capital, net revenue retention above 100% is among the most valued signals in a private SaaS.

- Efficiency: growing while burning little cash is worth more than growing at any cost.

The Rule of 40 is the established way to synthesize that trade-off: it adds the growth rate to the margin, and the ideal result lands at or above 40. The private SaaS survey by KeyBanc Capital Markets uses metrics of this kind to separate the companies that combine pace and discipline, exactly the ones that capture the highest multiples.

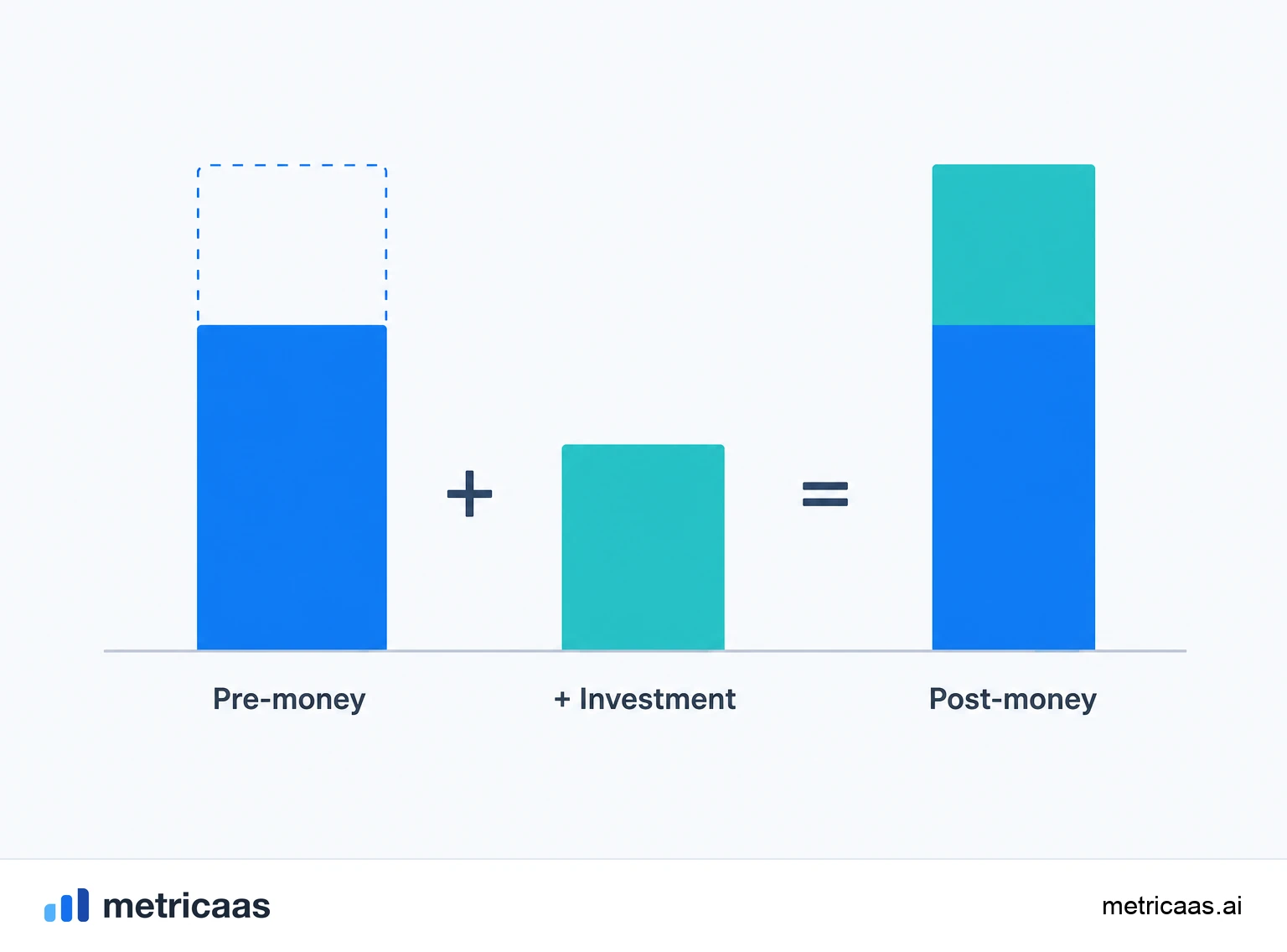

Pre-money and post-money

In an investment round, valuation shows up in two forms that cannot be confused. The pre-money is what the company is worth before receiving the investment. The post-money is the pre-money plus the money that came in.

- Post-money = pre-money + investment.

- Example: pre-money of $8 million, investment of $2 million, post-money of $10 million.

The distinction is not a detail: it decides the slice the investor takes. In the example above, the $2 million represent 20% of the post-money, so that is the stake the check buys. Confusing pre with post-money directly changes how much of the business the founder hands over for the same amount.

How valuation sets the investor equity

Valuation is not a vanity trophy: its practical effect is to define how much of the cap table changes hands. The math is direct: the investor slice is the investment divided by the post-money.

- Investor equity = investment / post-money.

- A $2 million investment on a $10 million post-money buys 20% of the company.

Every new round issues shares and re-splits the pie, which reduces the slice of those already in, an effect called dilution. That is why valuation matters so much to the founder: a higher pre-money means handing over less equity for the same money, preserving stake for the rounds to come.

Revenue multiple or discounted cash flow (DCF)

There are two broad logics for arriving at a valuation. The first is the revenue multiple, the shortcut we have seen: fast, market-driven and ideal for high-growth companies that are not yet profitable. The second is discounted cash flow (DCF), which projects the cash the company will generate in the future and brings it to present value.

In practice, DCF needs a stable cash history for the projections to make sense, something most growing SaaS companies do not yet have. That is why the ARR multiple dominates early rounds, while DCF gains weight as the company matures and cash becomes predictable. Good investors look through both lenses: the multiple says what the market pays today, DCF tests whether that price holds over the long run.

Frequently asked questions

The most used shortcut is to multiply ARR by a market multiple. A $10 million ARR at a 6x multiple gives a $60 million valuation. The multiple varies with growth, retention and efficiency.

It depends on the multiple. With $1 million of recurring revenue and a 5x multiple, valuation is around $5 million. High growth and retention push that multiple up.

Pre-money is the company value before the investment; post-money is pre-money plus the investment. Post-money = pre-money + investment.

It depends on the valuation and stage. 1% of a company valued at $100 million is worth $1 million, but later rounds dilute that stake. What matters is the absolute value and the growth potential.

Growth, retention and efficiency, synthesized by the Rule of 40. The more predictable and efficient the growth, the higher the multiple the market will pay.

A revenue multiple for high-growth companies that are not yet profitable; DCF when cash flow is predictable. Many investors use both lenses together.

Related concepts

ARR

ARR (Annual Recurring Revenue) is the annual recurring revenue of a SaaS: MRR multiplied by 12. It represents how much the company earns on a recurring basis over a year, counting only active subscriptions, with no one-off charges. It is the metric of choice for companies selling annual contracts and the standard language of investors.

Rule of 40

The Rule of 40 is a health check for SaaS companies that adds the revenue growth rate to the profit margin: the result should be 40% or higher. It balances two goals that usually compete, growing fast and turning a profit, into a single number. Above 40 the business combines growth and profitability sustainably; below it, a warning light comes on.

Cap table

A cap table, or capitalization table, is the record of who owns what in a company: founders, investors and the employee option pool, always adding up to 100%. It lists shares, percentages and share classes, and it is rewritten at every funding round, when new investment dilutes the existing holders. It is the basis for negotiating valuation and the term sheet.