Dilution: what equity dilution is and how it works across rounds

By Tiago Costa · Updated on July 9, 2026

Definition

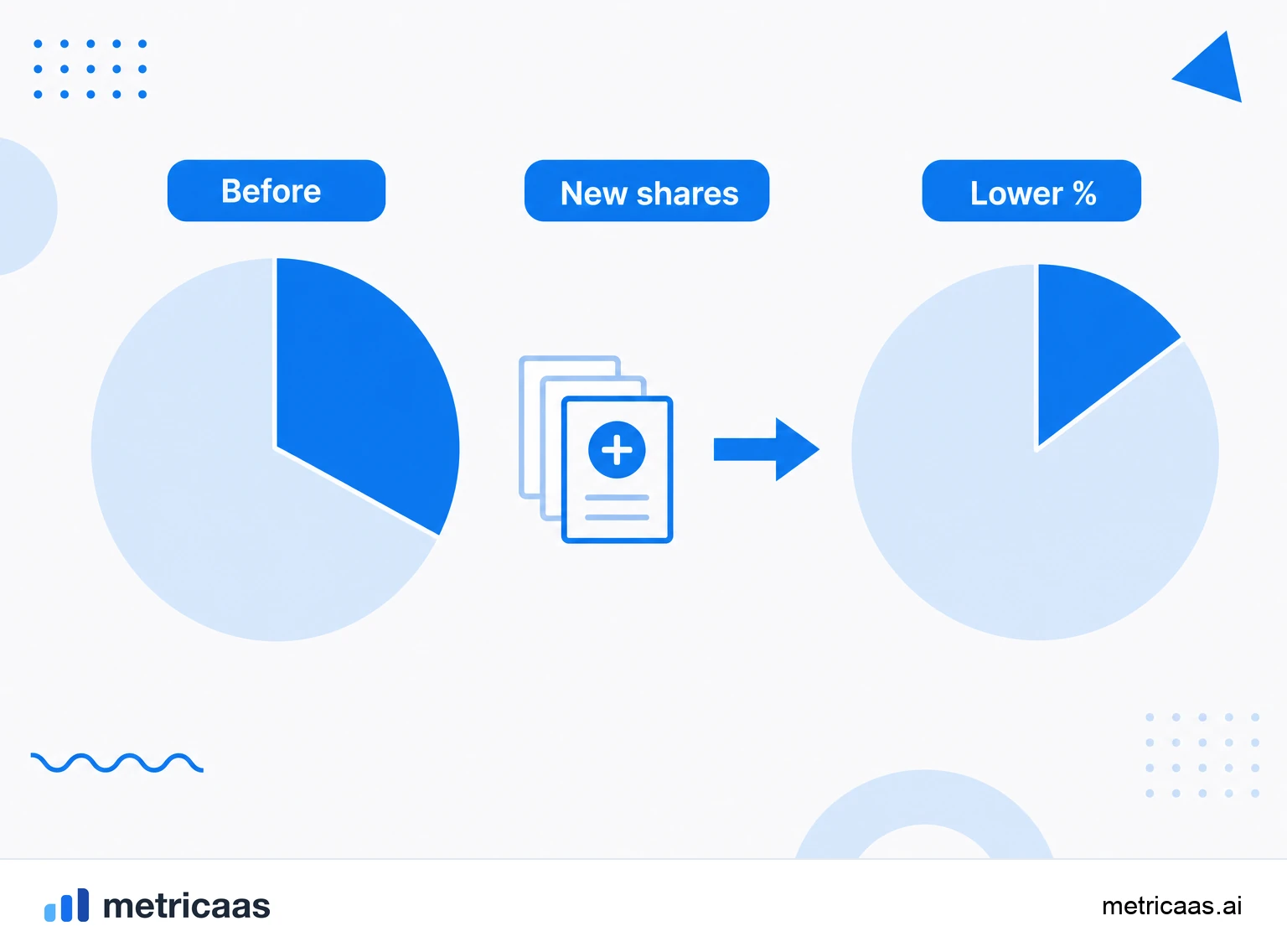

Dilution is the drop in existing owners' percentage when the company issues new shares, in a funding round or an option pool.

- Your share count does not change, but it becomes a smaller slice of the total.

- Each round dilutes on top of what was left: the effect is multiplicative.

- The goal is a smaller slice of a much bigger pie.

What dilution is

Dilution is the drop in existing owners' percentage when the company issues new shares. Nobody takes shares out of your hands: the total share count grows, so the same number of shares you hold now represents a smaller slice of the whole.

The classic image is the pie. After a round you own a smaller slice, but the bet is that the whole pie got much bigger. That is why dilution goes hand in hand with valuation: what matters is not only the percentage you keep, but how much the slice you kept is worth.

How dilution happens

Dilution shows up every time the company creates new shares: in a funding round, when a SAFE or convertible note converts, or when the option pool is set up for the team. The math is direct: add the new shares to the total and recompute each owner's percentage.

A simple example. Say the founders own 100% of the company. An investor puts in capital in exchange for 20% of the business: the company issues new shares equal to 20% of the post-round total, and the founders go from 100% to 80%. Their share count did not change, but their slice did. All of this is recorded in the cap table, which now shows who owns what after the issuance.

The option pool and the pool shuffle

Much of a founder's dilution comes not from the investor but from the option pool, the block of shares set aside to hire and retain the team. When that pool is created or topped up, new shares enter the count and everyone already on the table gets diluted.

The detail that catches many people is the pool shuffle: investors usually require the pool to be created before the round, inside the pre-money valuation. In practice, that means only the founders pay for it. If a 20% investment comes with a 10% pool built pre-round, founders do not land at 80% but at around 70%, because they absorb the dilution from the pool on their own.

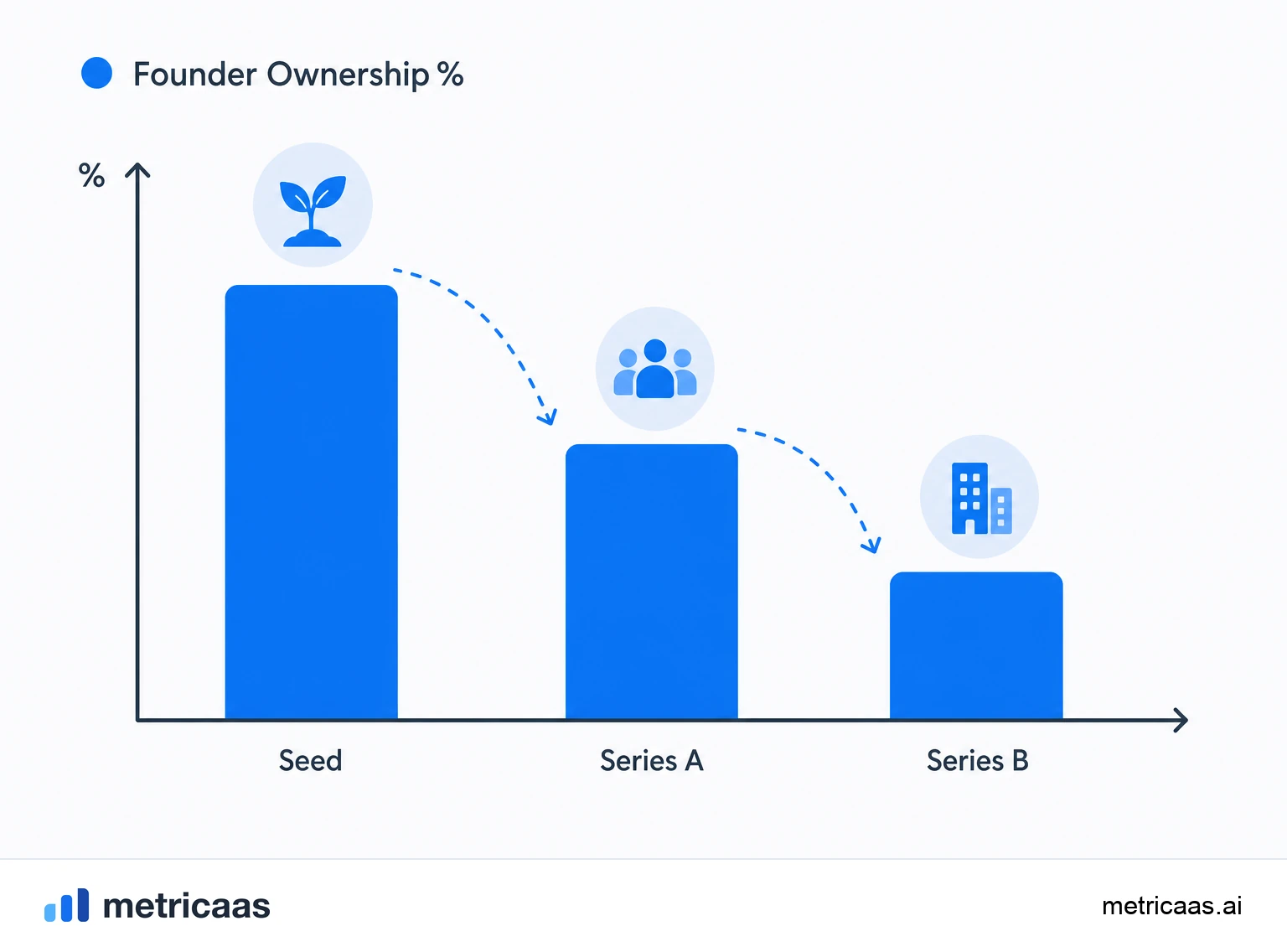

Cumulative dilution across rounds

Each round dilutes on top of what was left from the previous one, so the effect is multiplicative, not additive. If you keep 80% after the seed and then dilute another 20% in Series A, you do not end at 60%: you end at 80% of 80%, that is, 64%. A following 15% round takes you to around 54%.

That is why, by the later rounds, the founding team commonly owns a minority of the company it created. It is not a sign of failure: investors such as a16z have shown that the erosion of founder ownership is the rule, and what decides the outcome is the size of the pie at the end, not the percentage on its own. Planning that path from the start avoids surprises at the negotiating table.

Anti-dilution provisions

Anti-dilution provisions protect investors, not founders. They kick in when the company does a down round, a raise at a lower valuation than the previous one, and adjust the conversion price of the investor's preferred shares to offset the drop.

There are two families. Weighted average is the most common and the milder one: it adjusts the price taking the size of the new issuance into account. Full ratchet is aggressive: it reprices as if the investor had come in at the lowest price, shifting heavy dilution onto founders and common shareholders. Understanding which clause is in the term sheet is essential before signing.

A smaller slice of a bigger pie

Dilution is not the villain of the story. Raising capital and handing out options to attract talent are exactly the levers that make the pie grow. The goal is not to avoid dilution at any cost, but to make sure every slice given away in exchange for money or people is worth it.

In practice, that means negotiating a fair valuation (the higher it is, the less you dilute for the same check), sizing the option pool to what the team actually needs, and avoiding rounds that are too big too early. Accelerators such as Y Combinator repeat the same advice: raise what you need to reach the next milestone, not more, and protect your ownership for the stages where it matters most.

Frequently asked questions

It is the drop in existing owners' percentage when the company issues new shares, usually in a funding round or when creating the option pool. Your share count does not change, but it now represents a smaller slice of the total.

The company creates new shares and gives them to investors or to the option pool. With more shares in the total, each existing owner's percentage falls, even if the company's value rises.

Divide the new shares issued by the total shares after the round. If an investor receives 20% of the post-round total, founders who held 100% now hold 80%.

It is an investor protection that adjusts the conversion price of preferred shares in a down round. Weighted average is the most common version; full ratchet is the most aggressive and dilutes founders even more.

Not necessarily. You end up with a smaller slice, but of a pie that ideally got much bigger. What matters is the value of your stake, not the percentage alone.

It varies a lot, but since each round dilutes on top of what was left, the founding team commonly holds a minority after several raises. The size of the pie at the end is what decides whether it was worth it.

Related concepts

Cap table

A cap table, or capitalization table, is the record of who owns what in a company: founders, investors and the employee option pool, always adding up to 100%. It lists shares, percentages and share classes, and it is rewritten at every funding round, when new investment dilutes the existing holders. It is the basis for negotiating valuation and the term sheet.

Valuation

Valuation is the estimate of what a company is worth at a given moment. In SaaS, the most common shortcut is a multiple on ARR, and that multiple rises or falls with growth, retention and efficiency, synthesized by the Rule of 40. Valuation also sets how much equity an investor gets for their check, separating pre-money (before the check) from post-money (after).

Down round

A down round is a funding round raised at a lower valuation than the previous one. It signals that the market or the company performance did not hold up the old price, dilutes shareholders more, and can trigger anti-dilution provisions. Even so, it is sometimes the rational alternative to running out of cash, especially when the runway tightens and the prior valuation was stretched too far.