Net income: what it is, how to calculate it and how it differs from EBITDA

By Tiago Costa · Updated on July 9, 2026

Definition

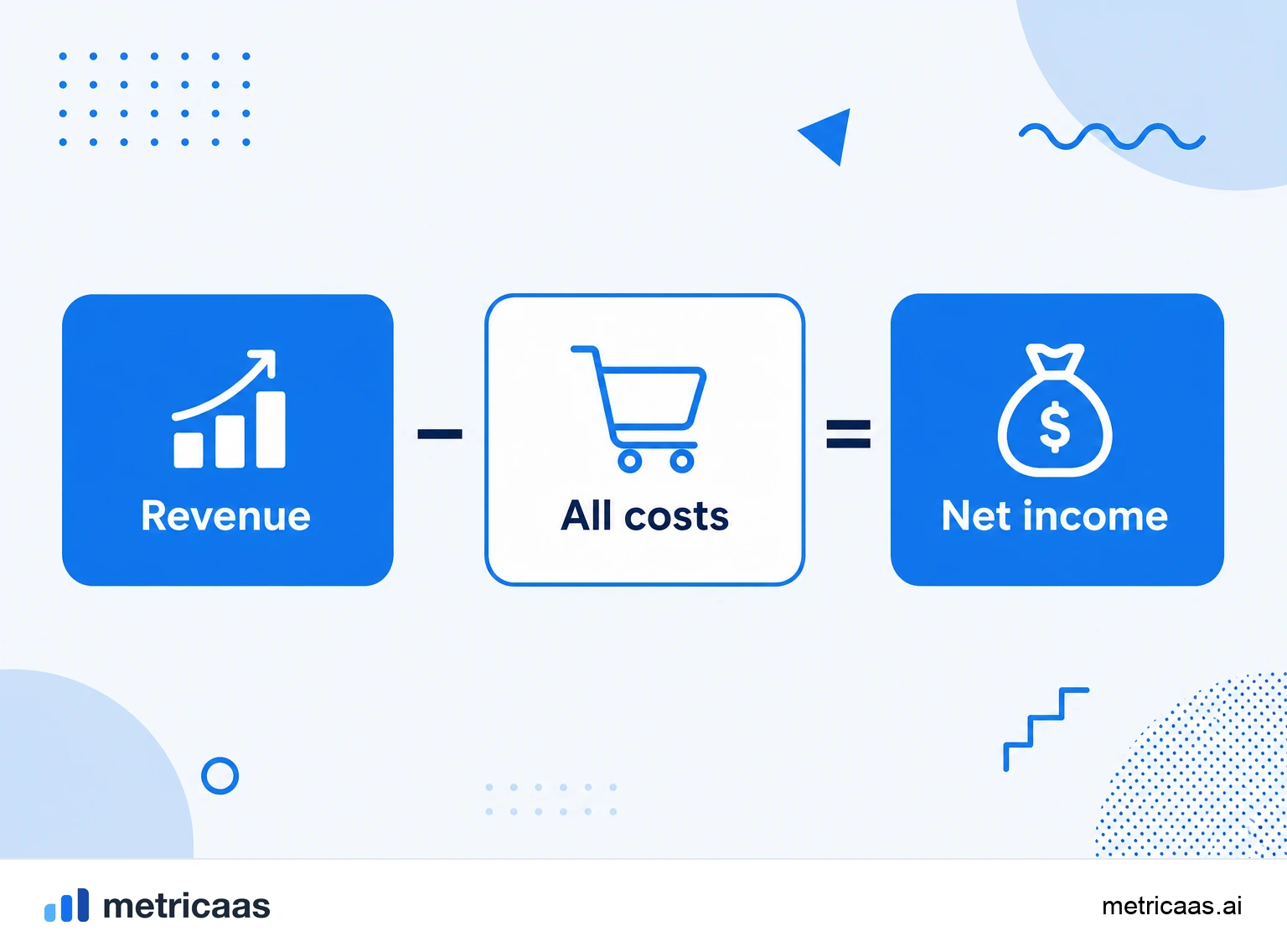

Net income is what is left of revenue after all costs, expenses, interest and taxes: the last line of the income statement.

- It is the final accounting profit, not cash in the bank.

- It differs from EBITDA, which ignores interest, taxes, depreciation and amortization.

- Many growth-stage SaaS run in the red by choice.

What net income is

Net income is the last line of the income statement, the famous bottom line: what is left of revenue after subtracting absolutely everything, cost of services, operating expenses, interest and taxes. It is the final accounting profit, the number that directly answers whether the company made or lost money in the period.

It starts at the top of the income statement, with revenue, and shrinks line by line down to the bottom. That is why net income sums up, in a single figure, the efficiency of the whole business: pricing, cost of delivery, expense structure and tax burden. A SaaS can post excellent gross profit and still close the year in the red if it overspends on sales, marketing and product.

How to calculate net income

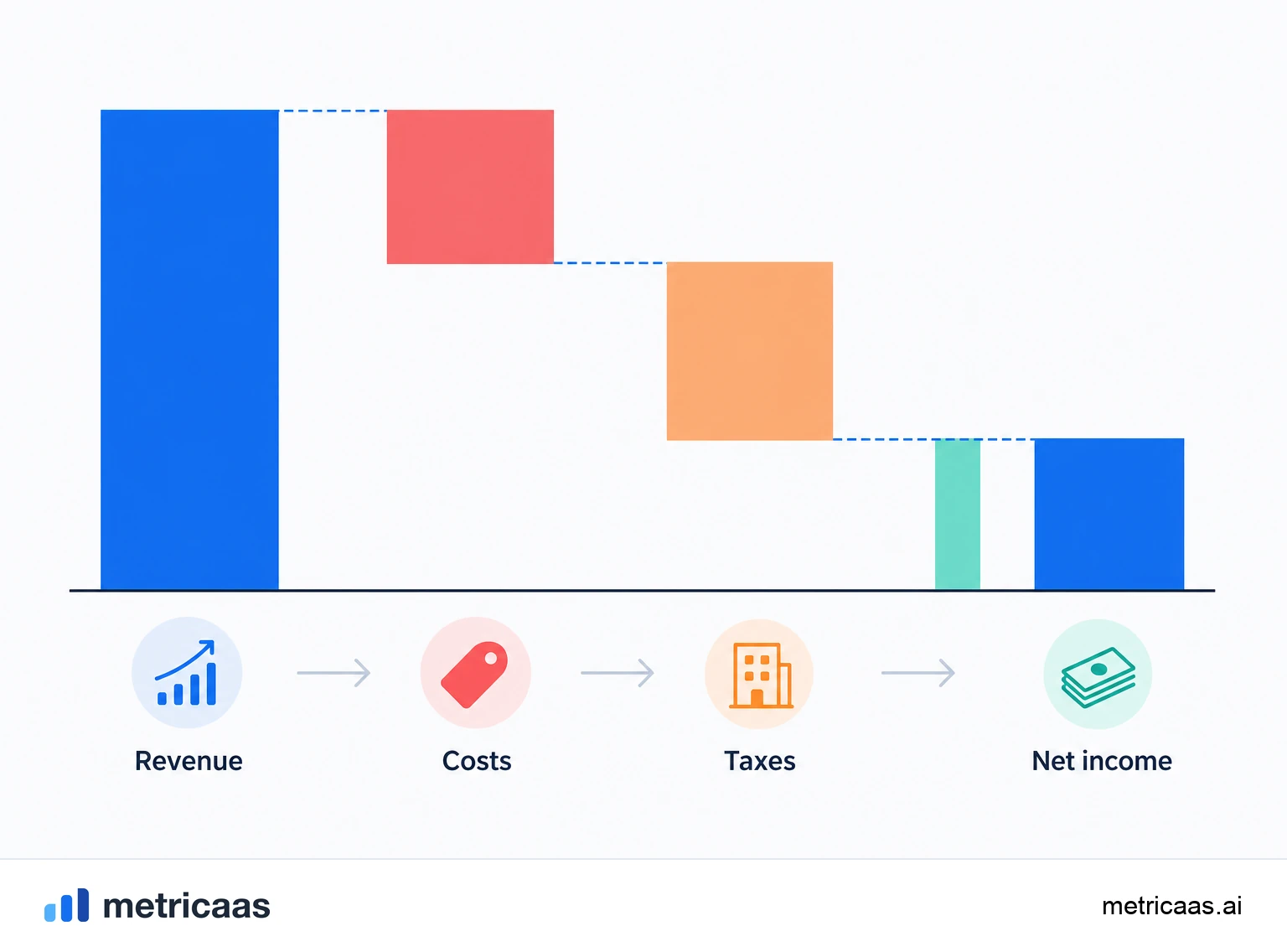

The calculation is a cascading subtraction that runs down the income statement from top to bottom, peeling off a block of cost at each step.

- Net revenue minus cost of services (COGS) gives gross profit.

- Gross profit minus operating expenses (sales, marketing, R&D, general and administrative) gives operating income.

- Operating income minus interest, plus or minus financial items, gives pre-tax income.

- Pre-tax income minus taxes gives net income.

As a direct formula: net income equals total revenue minus all costs, all expenses, interest and taxes. Example: a company with $10 million in revenue, $2 million in COGS, $6 million in operating expenses, $300k in interest and $400k in taxes closes with $1.3 million in net income, a net margin of 13%.

Net income, EBITDA and operating margin

Net income is the most complete of the profit measures and, for that reason, the smallest of them. It is often confused with EBITDA and with operating margin, but each one cuts the income statement at a different point.

- Operating margin: stops at operating income, before interest and taxes.

- EBITDA: excludes interest, taxes, depreciation and amortization, approximating operating cash generation.

- Net income: includes everything, it is the final line.

Because it carries depreciation, amortization, interest on debt and the tax bite, net income is usually much smaller than EBITDA. A SaaS can report positive EBITDA and negative net income at the same time, because amortization of capitalized software and interest still weigh below the operating line.

Net income is not cash: accrual vs cash

A classic mistake is treating net income as money in the bank. It is not. Net income follows accrual accounting: revenue is recognized when the service is delivered, not when the customer pays, and expenses are booked in the period they occur, not when they are disbursed.

A SaaS that charges an annual plan upfront receives the cash today but recognizes the revenue month by month over the twelve months. That is why cash flow can be positive while net income is still negative, or the other way around. Non-cash expenses such as depreciation and amortization reduce profit without taking money out of the pocket, and it is precisely this gap that the cash flow statement exists to reconcile.

Why many SaaS run negative net income

Seeing a growth-stage SaaS with negative net income is rarely a sign of illness. It is, almost always, a choice. The economics of recurring revenue reward whoever invests early: the cost of acquiring a customer is paid at once, but the revenue arrives spread over years of subscription.

While the company accelerates sales, marketing and product to capture market, those expenses show up in full in the quarter income statement, while the revenue they generate only matures later. The result is negative net income by design, betting that the recurring base and retention will outrun the investment. McKinsey, Bessemer and a16z have long described this logic of trading short-term profit for growth, as long as the unit economics work. The private SaaS survey by KeyBanc Capital Markets documents how these companies balance growth and margins as they mature.

The path to GAAP profitability

GAAP profitability means positive net income under the full accounting rules, with no convenient adjustments that dress up the result. It is the proof that the model stands on its own, without depending on funding rounds to pay the monthly bill.

The path combines predictable levers: scaling recurring revenue faster than expenses, defending operating margin, improving retention to dilute acquisition cost, and capturing efficiency as the structure gains scale. The industry informal ruler is the Rule of 40, which adds growth and margin: the more the company matures, the more the market demands that net income climb out of the red and that the promise of recurring revenue turn into real cash.

Frequently asked questions

It is the last line of the income statement, the bottom line: what is left of revenue after subtracting all costs, operating expenses, interest and taxes. It is the final accounting profit of the period.

Sum total revenue and subtract all costs, all operating expenses, interest and taxes. What remains is net income, and divided by revenue it gives the net margin.

After. Taxes are the last deduction on the income statement, so net income is already net of tax. Pre-tax income is the line just above it.

Gross profit is revenue minus cost of services, measuring product margin. Net income also subtracts operating expenses, interest and taxes, it is the final line.

Because they reinvest in sales, marketing and product to grow. Those expenses show up in full today, while the recurring revenue they generate only matures over years.

No. Net income follows accrual accounting and includes non-cash expenses like depreciation. Cash flow measures the money that actually comes in and goes out. The two can have opposite signs.

Related concepts

Gross profit

Gross profit is revenue minus COGS, the direct cost of producing and delivering the product or service. It is the first profit line on the income statement, taken before operating expenses, interest and taxes. Divided by revenue, it gives the gross margin, which in SaaS tends to be high because the cost of serving each additional customer is low.

EBITDA

EBITDA (earnings before interest, taxes, depreciation and amortization) measures the result a company generates from its operations, before decisions about financing, taxation and how past investments are accounted for. It starts from operating profit and adds depreciation and amortization back, approximating operating cash generation and letting you compare companies with different capital structures. It is not cash flow: it ignores capex and changes in working capital.

Operating margin

Operating margin is operating profit divided by revenue: how much of each dollar of revenue is left after paying the cost of service (COGS) and operating expenses (OPEX), before interest and taxes. It measures the profitability of the operation itself, with no effect from capital structure or taxes. In SaaS, it is the profitability component that adds to growth in the Rule of 40.