EBITDA: what it means, how to calculate it and why it is not cash flow

By Tiago Costa · Updated on July 9, 2026

Definition

EBITDA is earnings before interest, taxes, depreciation and amortization: it starts from operating profit and adds depreciation and amortization back.

- Approximates the cash generated by operations.

- Makes companies with different capital structures comparable.

- It is not cash flow: it ignores capex and working capital.

What EBITDA is

EBITDA stands for earnings before interest, taxes, depreciation and amortization. It measures how much profit a company generates from its core operations, before the effects of how it is financed (interest), where it is taxed (taxes) and how it accounts for past investments (depreciation and amortization).

By stripping out those four items, EBITDA aims to isolate operating performance. It approximates the cash a business produces from running its operations and makes it easier to compare companies that carry different levels of debt or invest in assets at different times.

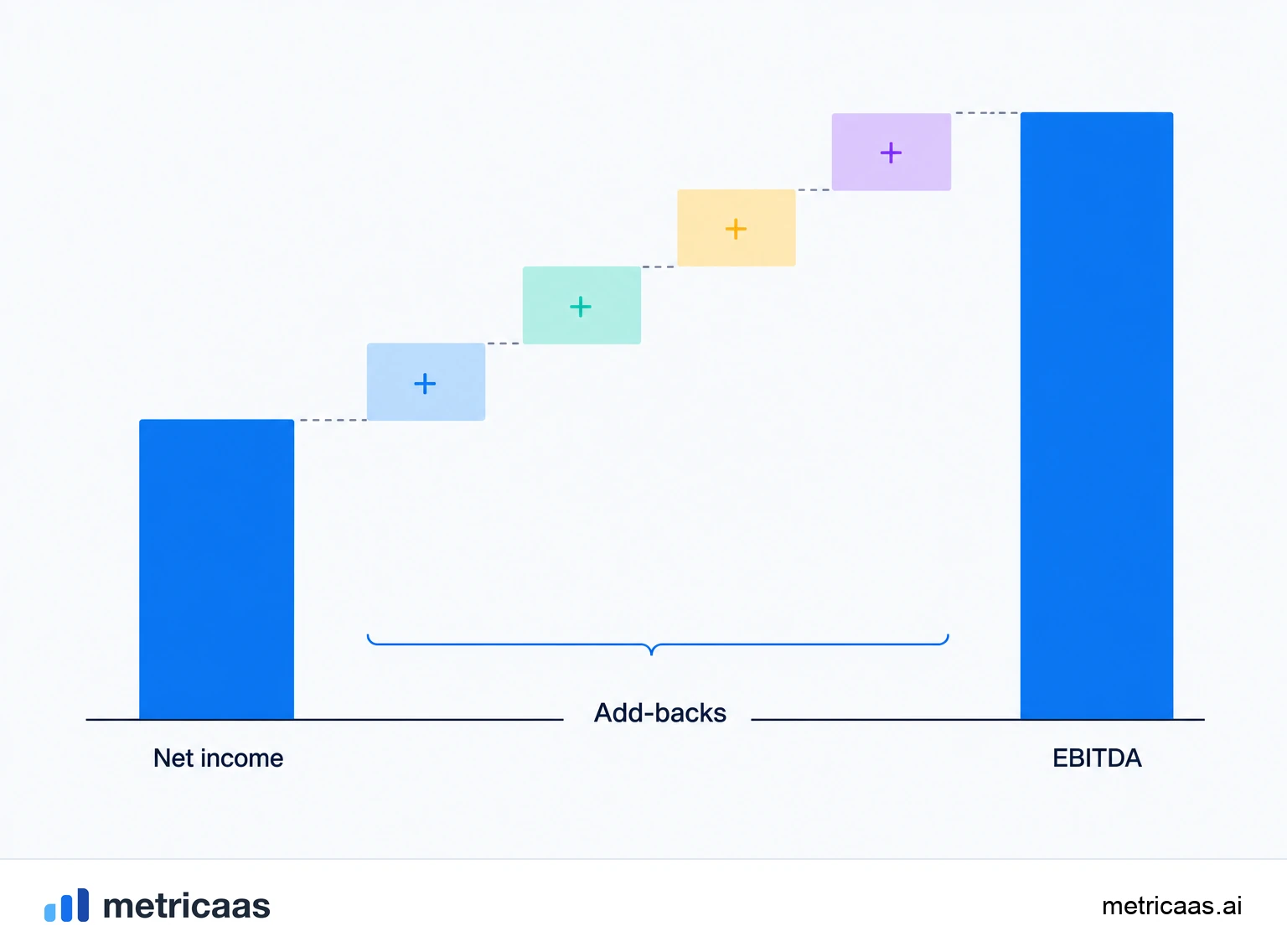

How to calculate EBITDA

There are two equivalent ways to reach EBITDA. The top-down path starts from operating profit (also called EBIT) and adds depreciation and amortization back. The bottom-up path starts from net income and adds back taxes, interest and depreciation and amortization.

- EBITDA = operating profit + depreciation + amortization.

- EBITDA = net income + taxes + interest + depreciation + amortization.

Example: a company with $100k of net income, $40k of taxes, $30k of interest and $80k of depreciation and amortization has an EBITDA of $250k. The same result comes from its $170k of operating profit plus $80k of depreciation and amortization. On $1 million of revenue, that is a 25% EBITDA margin.

Why depreciation and amortization are added back

Depreciation and amortization are non-cash charges. They spread the cost of assets bought in the past, machines, software, acquired intangibles, across several years, even though no cash leaves the business in the period. Adding them back removes an accounting effect that says little about how the operation is performing today.

Removing interest and taxes serves a related purpose. Interest reflects the capital structure, how much debt a company chose to take on, and taxes reflect the jurisdiction it operates in. Neither is about operating quality. That is what lets EBITDA sit close to operating margin while making two companies with very different financing comparable on the same footing.

EBITDA is not cash flow

The most common mistake is treating EBITDA as cash flow. It is not. EBITDA ignores capital expenditures, the cash a company spends to buy or replace assets, and it ignores changes in working capital, the cash tied up in receivables, payables and inventory. A business can post a healthy EBITDA and still burn cash.

To see real cash generation you need to keep going: subtract capex and working capital changes to reach free cash flow, and read the full cash flow statement. EBITDA is a proxy for operating cash generation, useful and quick, but it is a proxy, not the cash itself.

Adjusted EBITDA

Adjusted EBITDA goes one step further and removes items management considers one-off or non-operational: restructuring costs, litigation, stock-based compensation, gains or losses on asset sales, or expenses tied to an acquisition. The goal is to show the recurring earning power of the business without the noise of unusual events.

The catch is that these adjustments are discretionary. What one company calls a one-off, another books as a normal cost, so adjusted EBITDA can be stretched to flatter a weak quarter. This is why investors like Warren Buffett have long been skeptical of leaning on EBITDA, and especially adjusted EBITDA, in place of real earnings. Read the adjustments line by line before trusting the number.

EBITDA in SaaS

Software has very low marginal cost, so a mature SaaS can reach EBITDA margins well above what heavy-asset industries manage. But early-stage SaaS often runs a thin or negative EBITDA on purpose, reinvesting every dollar into growth. That is why profitability is usually read together with growth rather than in isolation.

The Rule of 40 captures that balance: growth rate plus profit margin (often an EBITDA or free cash flow margin) should clear 40%. The context keeps expanding, with Gartner projecting worldwide spending on SaaS applications approaching $300 billion in 2025, which is why investors, and consultancies like McKinsey and Bain, still lean on EBITDA multiples to value these businesses even as the mix of growth and profit shifts.

Frequently asked questions

It tells you how profitable the core operations of a company are, before interest, taxes, depreciation and amortization. It approximates operating cash generation and lets you compare businesses with different debt and tax situations.

No. Net profit already subtracts interest, taxes and depreciation and amortization. EBITDA adds those items back to isolate operating performance, so it is usually higher than net profit.

EBITDA = operating profit + depreciation + amortization. A company with $170k of operating profit and $80k of depreciation and amortization has an EBITDA of $250k.

A 20% EBITDA margin is often seen as solid across many industries, but it depends on the sector. A mature SaaS usually clears that comfortably thanks to the low cost of serving software. Compare against peers in the same market.

Warren Buffett has been openly skeptical of EBITDA, arguing that depreciation is a real cost and that leaning on EBITDA can hide the capital a business truly consumes. He prefers to look at earnings and cash flow.

It is EBITDA after removing items management treats as one-off or non-operational, such as restructuring, litigation or stock-based compensation. It can clarify recurring earning power, but the adjustments are discretionary and deserve a close read.

Related concepts

Operating margin

Operating margin is operating profit divided by revenue: how much of each dollar of revenue is left after paying the cost of service (COGS) and operating expenses (OPEX), before interest and taxes. It measures the profitability of the operation itself, with no effect from capital structure or taxes. In SaaS, it is the profitability component that adds to growth in the Rule of 40.

Cash flow

Cash flow is the difference between the money coming into a company and the money going out over a period. It splits into operating, investing and financing, and it is not profit: cash is what actually moves through the account. In SaaS, billing annual contracts upfront brings cash forward relative to recognized revenue.

Free cash flow

Free cash flow (FCF) is the cash left from operations after paying for capital investments (capex). It is the money truly available to pay down debt, reward investors or reinvest in growth. A SaaS that generates positive FCF funds itself and depends less on raising rounds.