Operating margin: what it is, how to calculate and analyze it

By Tiago Costa · Updated on July 9, 2026

Definition

Operating margin is operating profit divided by revenue, that is, what is left after the cost of service and operating expenses, before interest and taxes.

- Formula: operating profit (EBIT) divided by revenue.

- It sits between gross margin and net margin on the income statement.

- It feeds the Rule of 40 as the profitability component.

What operating margin is

Operating margin measures how much of each dollar of revenue turns into operating profit, that is, the result of the operation after paying the direct cost of delivering the service (COGS) and the operating expenses of selling, supporting and building the product (OPEX), but before interest and taxes.

By leaving out capital structure and the tax burden, it isolates the profitability of the operation itself. Two companies with the same product can post different net profits because of debt or taxes, but operating margin shows which of the two runs more efficiently at the core of the business. That is why analysts use it to compare the operational health of similar companies.

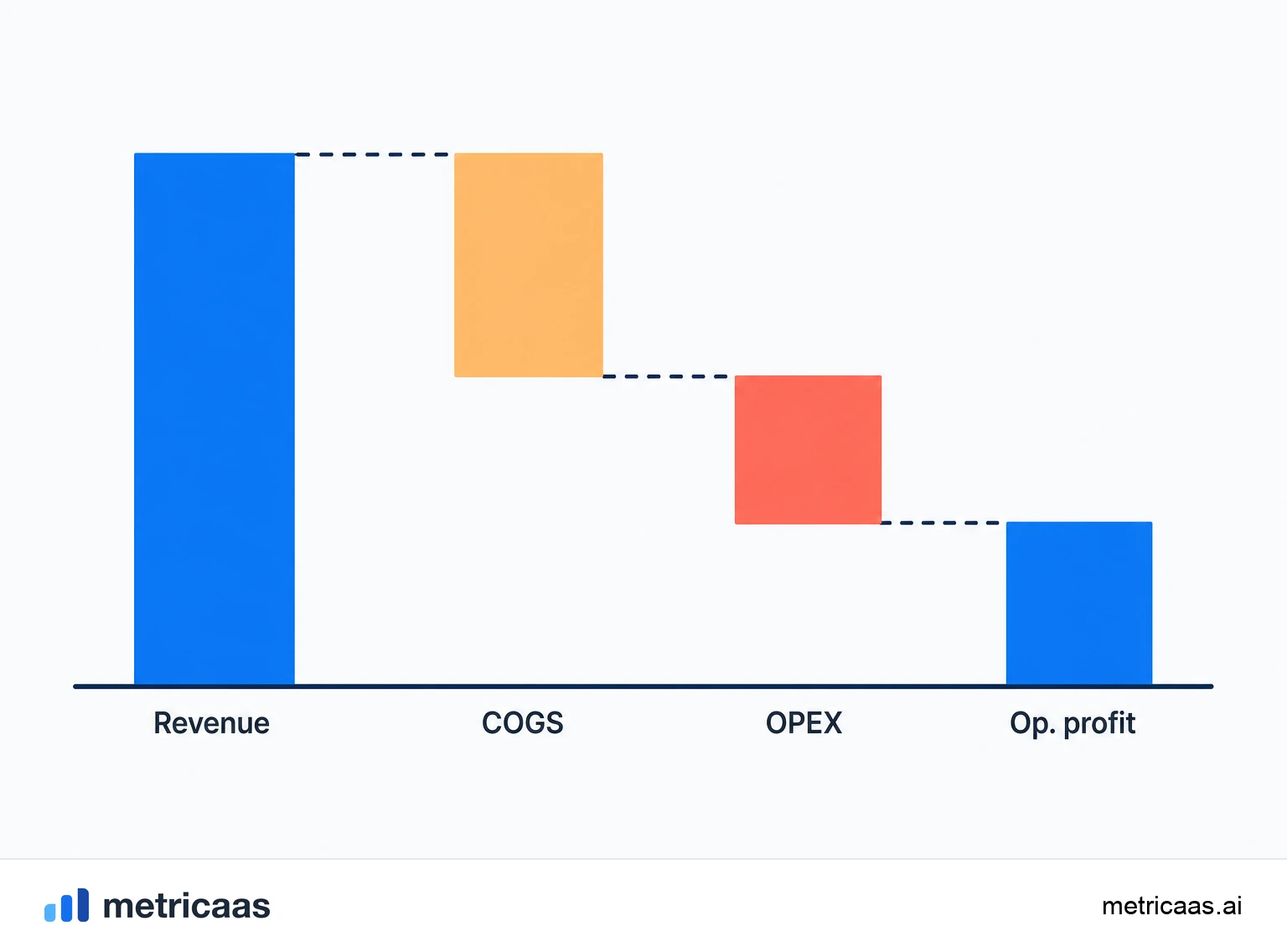

How to calculate operating margin

The formula is direct: operating margin = operating profit / revenue. On the income statement, you start from revenue, subtract COGS to reach gross profit (the base of gross margin) and then subtract OPEX to reach operating profit, also called EBIT.

- Revenue minus COGS = gross profit.

- Gross profit minus OPEX (sales and marketing, R&D, G&A) = operating profit (EBIT).

- Operating profit divided by revenue = operating margin.

Example: a company with $10 million in revenue, $2 million in COGS and $6 million in OPEX has $2 million in operating profit and a 20% operating margin. It is worth separating this from contribution margin, which looks at revenue minus variable costs per customer or product, a more granular cut than the company-wide operating margin.

Operating, gross and net margin

On the income statement, the margins form a cascade from top to bottom. Gross margin removes only COGS and shows delivery efficiency. Operating margin also removes OPEX and shows the efficiency of running the whole business. Net margin removes interest and taxes on top of that and shows what is actually left for shareholders.

In SaaS it is common to see gross margin of 70% to 80% and still a low or negative operating margin, because heavy spending on sales, marketing and R&D consumes almost all of the gross profit during the growth phase. Reading the three margins together avoids wrong conclusions: a high gross margin does not guarantee a profitable operation, and it is operating margin that reveals whether the whole machine finishes in the black.

Operating margin and EBITDA: the difference

EBITDA and operating margin are close relatives, but not the same. The operating profit (EBIT) in the numerator of operating margin already deducts depreciation and amortization; EBITDA adds those two back. That is why EBITDA margin almost always looks higher than the operating margin of the same company.

The practical question is what you want to measure. Operating margin includes the wear of invested capital (depreciation and amortization), which brings it closer to the real cost of operating. EBITDA removes that effect to compare companies with different asset structures. In SaaS, where the heavy asset is usually capitalized software rather than machinery, the difference between the two margins comes mostly from the amortization of software and of acquired intangibles.

GAAP and non-GAAP operating margin in SaaS

In SaaS financials there are two operating margins living side by side. GAAP operating margin follows accounting rules to the letter. Non-GAAP operating margin excludes some items the company considers unrepresentative of the recurring operation, the most common being stock-based compensation and the amortization of intangibles acquired in mergers.

Stock-based compensation does not leave the bank account, but it is a real expense that dilutes shareholders, so the non-GAAP version usually shows a much higher margin than GAAP. Neither is the only correct one: GAAP is comparable and auditable; non-GAAP tries to reflect operating cash more closely. The important thing is to know which one is being quoted before comparing two companies, because the gap can reach tens of percentage points.

Operating margin in the Rule of 40

Operating margin is one of the most common ways to measure profitability inside the Rule of 40, the principle that the sum of a SaaS company revenue growth and profit margin should be 40% or more. A company growing 30% with a 15% operating margin sums to 45% and passes the test; another growing 50% with a -20% operating margin sums to 30% and fails.

The rule was born in the venture capital community and is used by funds such as Bessemer to balance growth and profitability instead of rewarding top line alone. The annual private SaaS survey by KeyBanc Capital Markets reinforces this shift, pointing to cost discipline and operational excellence among SaaS companies. In the Rule of 40 you can use operating margin, EBITDA margin or free cash flow margin; what does not change is the role of the margin as the counterweight to growth.

Frequently asked questions

It means how much of each dollar of revenue becomes operating profit. It is operating profit (revenue minus COGS and OPEX) divided by revenue, before interest and taxes, and it measures the profitability of the operation itself.

Operating margin = operating profit / revenue. Operating profit (EBIT) is revenue minus COGS and minus OPEX, before interest and taxes.

Start from revenue, subtract COGS to find gross profit, subtract OPEX to find operating profit (EBIT) and divide that operating profit by revenue.

Operating margin uses EBIT, which already deducts depreciation and amortization. EBITDA adds those two back, so EBITDA margin almost always appears higher than the operating margin of the same company.

For SaaS, 20% is a solid operating margin, typical of mature companies. During fast growth it is common for the margin to be low or even negative, so the number has to be read alongside the stage and the pace of growth.

GAAP follows accounting rules to the letter. Non-GAAP excludes items such as stock-based compensation and the amortization of acquired intangibles, which usually shows a much higher margin.

Related concepts

Gross margin

Gross margin is the share of revenue left after the direct cost of delivering the service: (revenue minus COGS) divided by revenue, as a percentage. Pure SaaS usually runs between 70% and 85% or more, and that headroom is what sustains the model, feeds LTV and funds reinvestment in growth.

Contribution margin

Contribution margin is revenue minus variable costs, measured per unit or in total. It is what each sale leaves over to cover fixed costs and, after that, become profit. Unlike gross margin, which subtracts all of COGS, it isolates only what changes with volume, which is why it underpins break-even analysis and pricing decisions.

EBITDA

EBITDA (earnings before interest, taxes, depreciation and amortization) measures the result a company generates from its operations, before decisions about financing, taxation and how past investments are accounted for. It starts from operating profit and adds depreciation and amortization back, approximating operating cash generation and letting you compare companies with different capital structures. It is not cash flow: it ignores capex and changes in working capital.