Involuntary churn: what it is, causes and how to recover with dunning

By Tiago Costa · Updated on July 9, 2026

Definition

Involuntary churn is cancellation caused by a payment failure, not a customer choice.

- The cause is usually the card: declined, expired, out of limit or blocked.

- The customer did not want to leave, so the revenue is recoverable.

- Fought with dunning: retries and card updates.

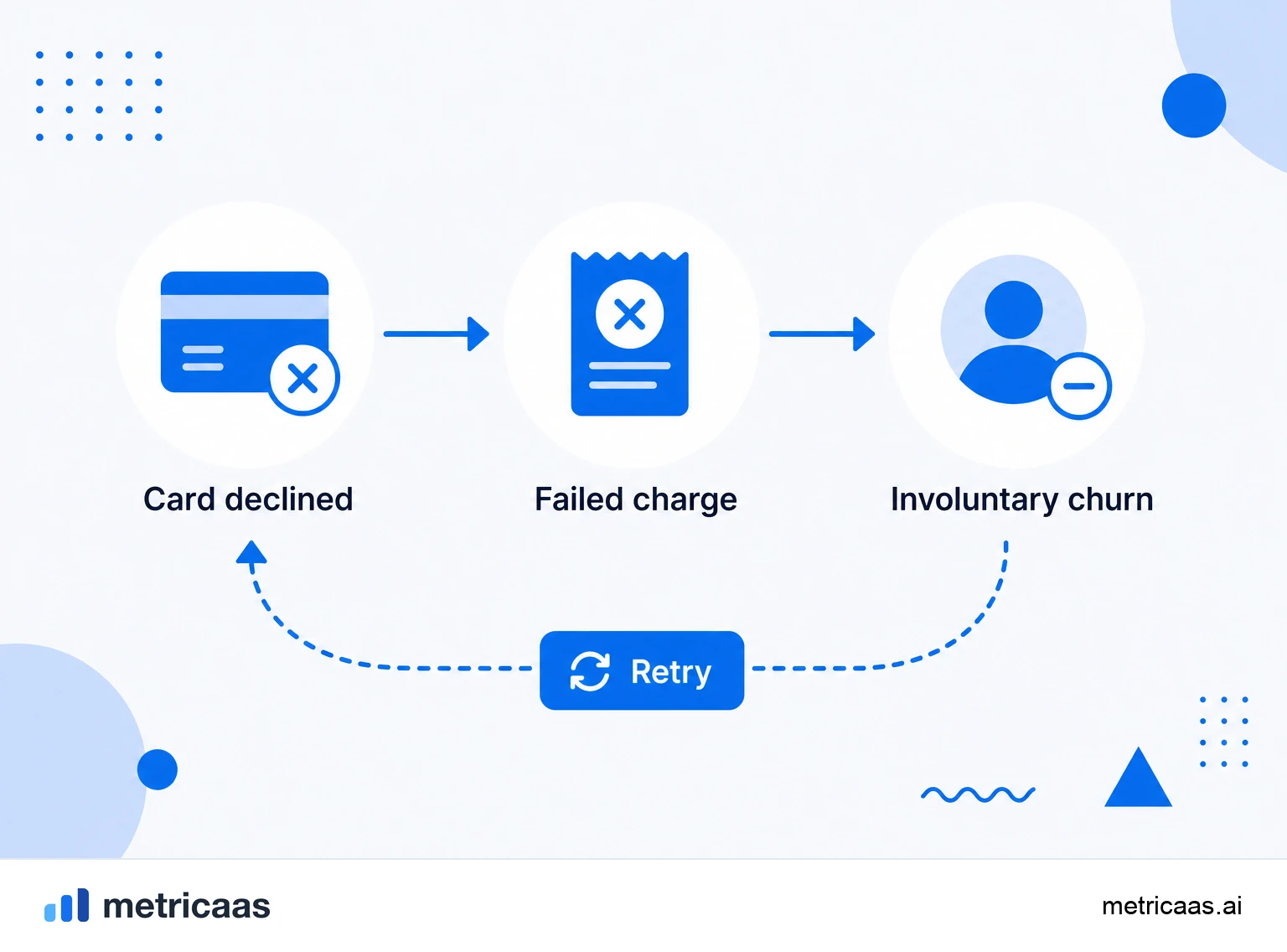

What involuntary churn is

Involuntary churn is the cancellation of a subscription caused by a payment failure, not by a customer decision. The customer still wants to use the product, but the charge does not go through: the card was declined, expired, hit its limit or the bank blocked the transaction. From the system point of view, the subscription drops; from the relationship point of view, the customer often never notices they left.

This distinction matters because it separates a product problem from a billing-operations problem. While total Churn mixes people who left on purpose with people who left by accident, isolating the involuntary part reveals revenue that is, in practice, still yours and that is usually recoverable with process, not with a discount.

Involuntary vs voluntary: the difference that changes strategy

Voluntary churn is when the customer decides to leave: they found it too expensive, saw no value, moved to a competitor or ended the project. Involuntary churn is when nobody decided to leave, but the payment failed. The cause is different, so the fix is different too.

- Voluntary: fought with product, value, onboarding and relationship.

- Involuntary: fought with billing infrastructure, retries and failure communication.

Treating both as the same thing makes a company spend energy in the wrong place: offering a discount to someone who only needed to update their card, or reworking the product to fix what was a gateway error. Measuring them separately is the first step to acting correctly.

Why the payment fails: the most common causes

Most involuntary failures come from a handful of recurring causes, almost all tied to the credit card, the dominant payment method in SaaS.

- Expired card: the validity ran out and the customer did not update the details.

- Insufficient funds or limit: the charge hits the card ceiling or a lack of balance.

- Issuer decline: the bank blocks it over suspected fraud, travel or an internal rule.

- Outdated data: number, CVV or address changed and the transaction does not validate.

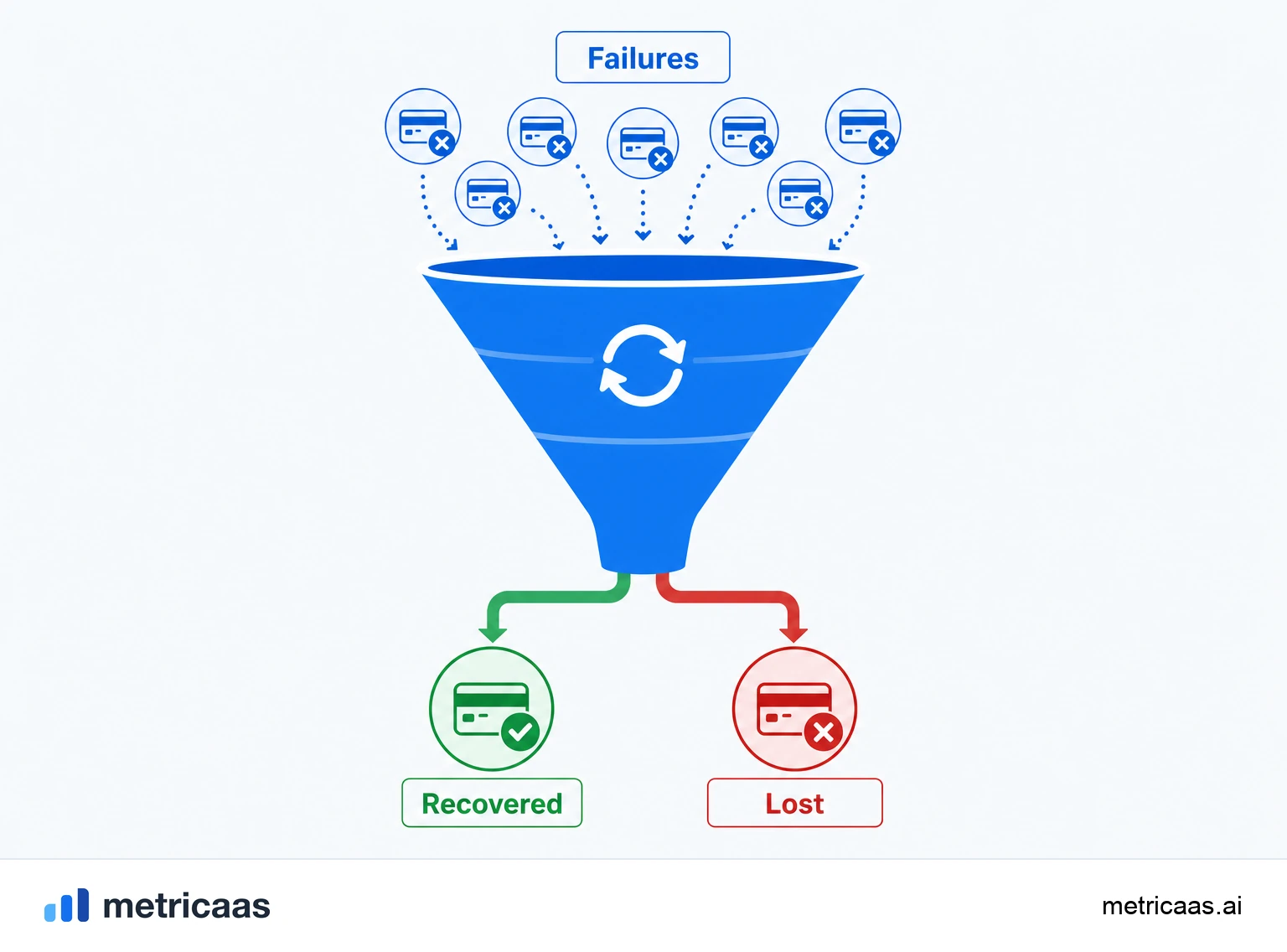

Many of these declines are temporary: a fresh attempt two days later goes through with no action from the customer. It is exactly this transient nature that makes involuntary churn so recoverable, as long as there is a process to retry at the right time.

How much it weighs in total churn

In subscription businesses, involuntary churn is rarely a footnote: it usually accounts for a meaningful slice of all cancellation, sometimes rivaling voluntary churn. Every failed payment that turns into a cancellation is lost MRR from a customer who never wanted to leave.

The impact goes beyond the month: because the customer was already paid and activated, losing them to an expired card throws away all the CAC spent to acquire them. According to SaaS Capital, revenue retention is one of the strongest drivers of a SaaS company value, and stopping the involuntary bleed is one of the cheapest ways to improve it.

Dunning and retries: how to recover

The main weapon against involuntary churn is dunning: the set of retries and messages that try to recover a failed payment before the subscription is actually cancelled. Instead of writing off the first decline, the system tries again at smart intervals and warns the customer.

- Automatic retries: repeat the charge on different days and times, when the odds of approval are higher.

- Email communication: tell the customer about the problem and ask them to update the card.

- Grace period: keep access active for a few days while recovery happens.

- Automatic card updater: use network services that fetch the new number when a card is reissued.

Well tuned, dunning recovers a good share of failures without the customer having to do anything. The opposite mistake exists too: overly aggressive retries annoy the customer and can turn involuntary churn into voluntary churn.

How to measure and reduce involuntary churn

Measuring starts by splitting, in the churn report, active cancellation from payment failure. Without that break, involuntary churn hides inside the total number and no one works on it. Once isolated, it becomes an operational target with clear levers.

- Track the recovery rate of failed payments, not just the churn rate.

- Reduce card-update friction, with a simple page and reminders before expiry.

- Test the retry schedule and the timing of the emails.

Because much of this loss is avoidable, involuntary churn is one of the rare places where you can improve retention by changing process, not product. It is cheap retention: winning back a customer who already wanted to stay costs far less than reconquering one who decided to leave.

Frequently asked questions

It is the cancellation of a subscription caused by a payment failure, such as a declined, expired or maxed-out card, rather than a customer decision to leave.

In voluntary churn the customer decides to cancel; in involuntary churn nobody decides to leave, but the payment fails. One is solved with product and value, the other with billing and retries.

With dunning: automatic retries at good times, emails asking to update the card, a grace period and automatic card updater services from the networks.

The most cited are customer churn, revenue churn (MRR) and, by cause, the split between voluntary and involuntary churn.

Because many card declines are temporary: a fresh attempt days later usually goes through with no action from the customer, who never wanted to cancel.

Related concepts

Churn

Churn is the loss of customers or revenue in a period. In a SaaS, it measures how many customers cancel (customer churn) or how much recurring revenue disappears (revenue churn). It is the metric that reveals whether growth is sustainable: the higher the churn, the more new sales you need just to avoid shrinking.

Voluntary churn

Voluntary churn happens when a customer actively decides to cancel the subscription, driven by price, low perceived value, a change of need or competition. It is the opposite of involuntary churn, which comes from payment failures. You fight it with activation, delivered value and product, not with billing.

MRR

MRR (Monthly Recurring Revenue) is the monthly recurring revenue of a SaaS: the sum of all active subscriptions normalized to a month. It is the core metric of a subscription business because it shows, predictably, how much the company earns on a recurring basis each month, without counting one-off charges.