Free cash flow: what FCF is and how to calculate it

By Tiago Costa · Updated on July 9, 2026

Definition

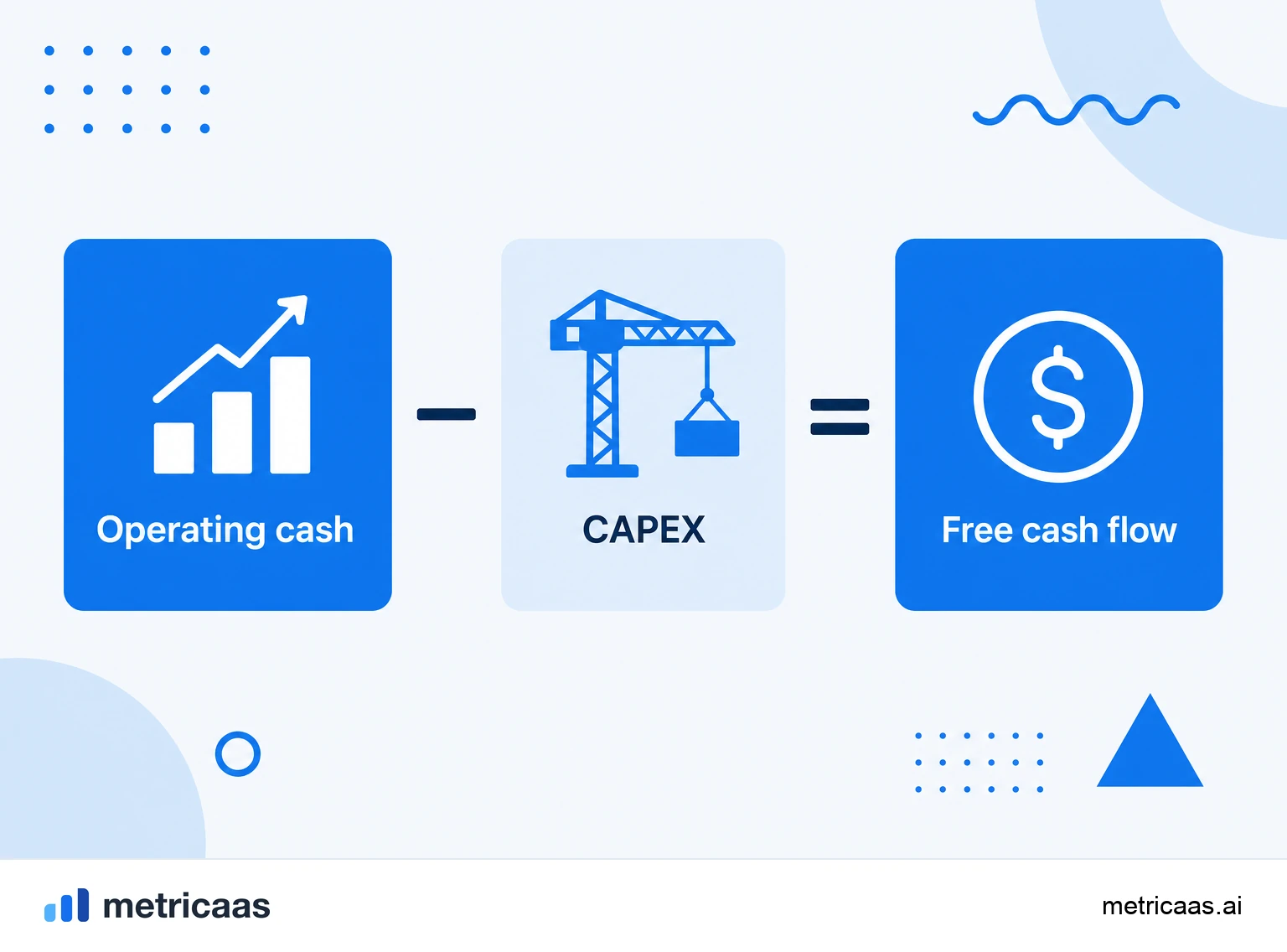

Free cash flow (FCF) is operating cash flow minus capital investments (capex): the money truly left over.

- Measures the cash available for debt, investors or reinvestment.

- FCF = operating cash flow minus capex.

- Positive FCF signals maturity: the business funds itself.

What free cash flow is

Free cash flow (FCF) is the cash a business generates from operations and that is left over after funding the investments needed to run and grow it. In other words, it is the money the company could hand to its owners, use to pay down debt or reinvest without straining the operation.

It starts from operating cash flow and subtracts capex, the spending on long-term assets. That is why FCF is more honest than accounting profit: showing a profit on the income statement is not enough, the cash actually has to remain after everything the business consumes to function.

How to calculate free cash flow

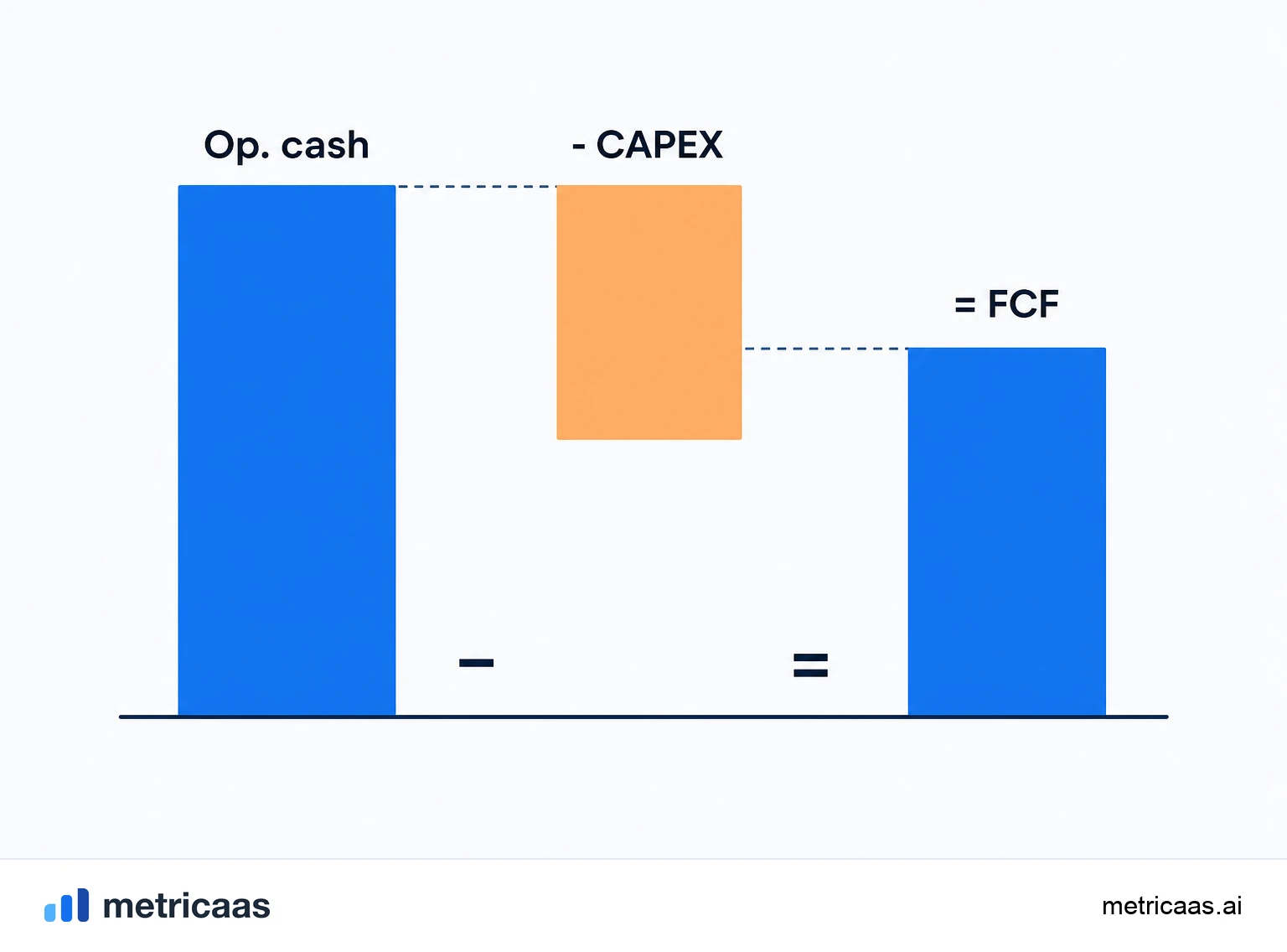

The most direct formula starts from the cash the operation generates and subtracts capital investments:

- FCF = operating cash flow - capex.

- Operating cash flow: the cash coming in from the operation after costs, expenses and the change in working capital.

- Capex: investments in long-term assets (equipment, infrastructure, capitalized development).

Example: if the operation generated $2 million of cash in the year and the company invested $300k in capex, FCF was $1.7 million. In SaaS, capex tends to be low, so the big cash drain is rarely machines: it is hiring, marketing and the change in working capital, which already flow through operating cash flow.

FCF, EBITDA and net income: what changes

All three measure "results", but at different layers. Net income is the accounting result after taxes, interest and depreciation. EBITDA is earnings before interest, taxes, depreciation and amortization, an approximation of operating generation. FCF goes further: it starts from real cash and still subtracts capex and the change in working capital.

The difference is practical. A company can have positive EBITDA and negative FCF if it invests heavily or burns cash financing customers. And it can have low net income (because of depreciation) yet strong FCF. That is why investors look at FCF to know how much money the business actually pockets, not how much it reports.

- Net income: the final accounting result, subject to non-cash items.

- EBITDA: a proxy for the operation, but it ignores capex, interest, taxes and working capital.

- FCF: the cash truly left over, the hardest to dress up.

FCF margin: what a good number looks like

FCF margin shows how much of each dollar of revenue turns into free cash: it is FCF divided by revenue. It answers a simple question: for every $100 that comes in, how much is really left after operating and investing?

In mature SaaS, double-digit FCF margins are a sign of efficiency, and the best companies pair growth with a rising FCF margin. The private SaaS survey by KeyBanc Capital Markets reinforces this focus on operational excellence and cash efficiency across the sector. Firms like Bessemer and McKinsey argue the same point: growth is necessary, but growing while generating cash is what sustains the business over the long run.

Unlevered vs levered FCF

There are two readings of FCF, and confusing them distorts the analysis. Unlevered FCF is free cash before the effect of debt: it measures the operation as if the company had no financing, useful for comparing businesses with different capital structures. Levered FCF is what remains after paying interest and debt repayments: the cash that actually stays with shareholders.

The distinction matters because two companies with the same operation can deliver very different cash to the owner, depending on how much they owe. Unlevered FCF assesses the quality of the operation; levered FCF assesses what is left after creditors. In SaaS, where most companies grow with little debt, the two tend to sit close together, but the gap widens as the company takes on credit.

Why FCF measures a SaaS company maturity

While it burns cash, a SaaS depends on rounds to keep existing. The turning point is positive FCF: from there, the operation starts to pay for itself and fund its own growth, and the company stops being hostage to the next investor cheque. That is why positive FCF is one of the most respected milestones of maturity.

FCF is the conceptual opposite of burn rate: while burn measures how much cash disappears each month, positive FCF measures how much is left. This shift has scale: according to Gartner, worldwide public cloud spending is set to approach $723 billion in 2025, a market large enough that generating cash, not just growing, has become the yardstick of quality. A SaaS that pairs growth with positive FCF proves the model closes its own accounts.

Frequently asked questions

It is the cash generated by the operation minus capital investments (capex): the money truly left over, available for debt, investors or reinvestment.

FCF = operating cash flow minus capex. If the operation generated $2 million and capex was $300k, FCF was $1.7 million.

Net income is an accounting result with non-cash items like depreciation. FCF starts from real cash and subtracts capex, showing how much money is actually left over.

No. EBITDA ignores capex, interest, taxes and the change in working capital. FCF subtracts all of it, so a company can have positive EBITDA and negative FCF.

FCF margin is FCF divided by revenue. In mature SaaS, double-digit margins signal efficiency, especially when they rise alongside revenue.

Unlevered FCF measures the operation before debt; levered FCF is what remains after interest and repayments, that is, the cash that stays with shareholders.

Related concepts

Cash flow

Cash flow is the difference between the money coming into a company and the money going out over a period. It splits into operating, investing and financing, and it is not profit: cash is what actually moves through the account. In SaaS, billing annual contracts upfront brings cash forward relative to recognized revenue.

EBITDA

EBITDA (earnings before interest, taxes, depreciation and amortization) measures the result a company generates from its operations, before decisions about financing, taxation and how past investments are accounted for. It starts from operating profit and adds depreciation and amortization back, approximating operating cash generation and letting you compare companies with different capital structures. It is not cash flow: it ignores capex and changes in working capital.

Burn rate

Burn rate is the speed at which a company consumes its cash, almost always measured per month. Gross burn adds up all the money going out; net burn subtracts the revenue coming in and shows what actually drains the cash. It is the denominator of runway: the lower the burn, the more time a startup has before it needs new capital.