Working capital: what it is, how to calculate it and why SaaS can run negative

By Tiago Costa · Updated on July 9, 2026

Definition

Working capital is current assets minus current liabilities: the short-term money to run the operation.

- Measures whether cash, receivables and inventory cover short-term obligations.

- Depends on the cash conversion cycle: receivables plus inventory minus payables.

- In SaaS with upfront billing, it is often negative in a healthy way.

What working capital is

Working capital is a company short-term financial cushion: everything it can turn into cash over the next few months minus everything it has to pay in the same period. In accounting terms, it is current assets (cash, short-term investments, receivables, inventory) minus current liabilities (suppliers, wages, taxes and debt due within a year). It is what keeps the operation turning without needing a fresh injection at every payroll.

Unlike profit, which shows up in the period result, working capital is a snapshot of the balance between what comes in and what goes out in the short term. A company can be profitable on paper and still seize up for lack of working capital, if the cash from sales is slow to arrive and the bills come due first. That is why it speaks directly to cash flow: one watches the balance, the other watches the movement.

How to calculate working capital

The formula is straightforward: working capital is current assets minus current liabilities. The result can be positive (there is slack) or negative (short-term obligations exceed short-term resources).

- Working capital = current assets - current liabilities.

- Current assets: cash, liquid investments, receivables and inventory.

- Current liabilities: payables to suppliers, wages, taxes and debt installments due within twelve months.

Example: a company with $800k in current assets and $500k in current liabilities has $300k of positive working capital. Many people also track the current ratio, which is the same comparison as a ratio (current assets divided by current liabilities); above 1 signals slack, below 1 signals strain. The absolute figure and the ratio tell the same story from different angles.

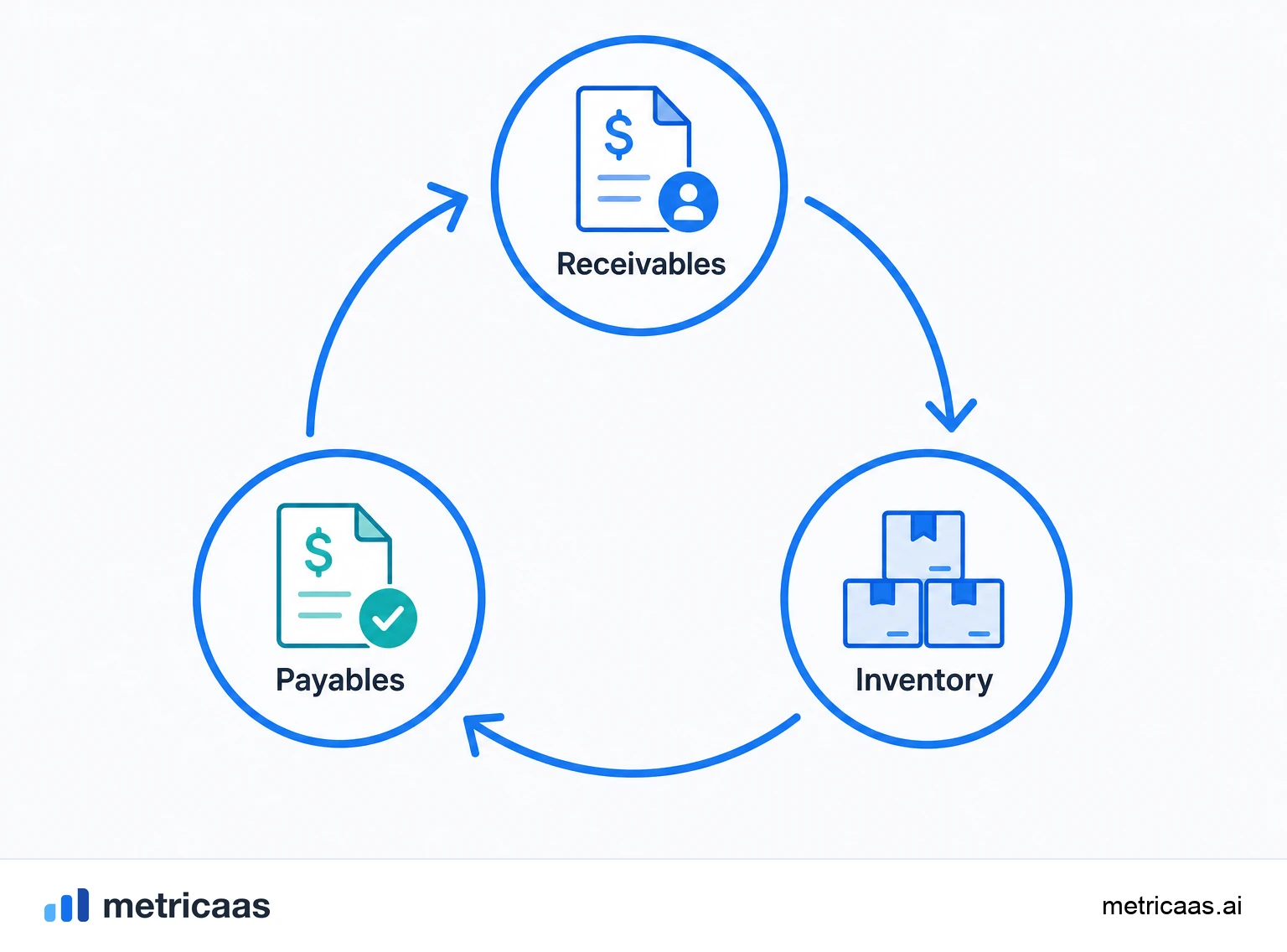

The cash conversion cycle

Working capital is not static: it breathes to the rhythm of the cash conversion cycle, the time between paying a supplier and getting paid by the customer. The longer that cycle, the more cash is trapped in the operation and the greater the working capital need.

The cycle has three gears: days of receivables (how long the customer takes to pay), days of inventory (how long the product sits) and days of payables (how long the company can defer paying suppliers). The intuition is simple: receivables + inventory - payables. Shortening the collection period, turning inventory faster or negotiating longer terms with suppliers compresses the cycle and frees up cash. McKinsey often treats managing this cycle as one of the most underrated levers of cash generation, because it improves liquidity without having to sell more or cut costs.

Why SaaS runs on negative working capital

In a well-run SaaS, the cash conversion cycle tends to be negative, and that is an advantage. The company bills the subscription upfront, often a full year at once, and only pays most of its costs (wages, infrastructure, commissions) over the following months. The customer funds the operation, not the other way around.

This is the effect of healthy negative working capital: because money comes in before it goes out, every new annual contract injects cash that can be reinvested in growth before the matching expense appears. It is one reason the subscription model scales so well and why the SaaS market keeps expanding; according to Gartner, worldwide public cloud spending is set to top $700 billion in 2025. The catch is not to confuse upfront cash with profit: part of it is revenue still to be delivered month by month, and spending it all at once accelerates the burn rate before the revenue has been recognized.

Deferred revenue: a liability that is good news

When a SaaS bills twelve months upfront, that money hits the bank, but in accounting it becomes deferred revenue, a current liability. It seems counterintuitive: why does a payment become a debt? Because the company still owes the service in the coming months; it recognizes the revenue gradually, as it delivers, and the portion not yet delivered stays on the books as an obligation.

In the working capital reading, that liability pulls the number down, and that is exactly where the good news hides. A large and growing deferred revenue means customers have prepaid for service the company will deliver at high margin over time. It is a liability that requires no cash outlay; it settles by shipping software. Investors read deferred revenue as an early signal of future free cash flow and of annual contracts on the rise, not as a short-term risk.

How to manage working capital in SaaS

Managing working capital in a SaaS is, at heart, managing the timing of cash. Because revenue arrives upfront, the focus shifts from "collect faster" to "do not let the model drift into positive by accident", which would happen if the company started selling mostly monthly plans or granting long payment terms.

- Encourage annual contracts with a discount: it pulls cash forward and lengthens deferred revenue.

- Bill before delivering, with auto-renewal, to keep the cycle negative.

- Control late payments and involuntary churn, which turn receivable revenue into a loss.

- Do not spend upfront cash as if it were profit: separate what is already delivered from what is still an obligation.

Well managed, working capital stops being a survival problem and becomes growth fuel. It connects to cash flow and the burn rate in one story: how long the company can grow on the money its own customers pay in advance, before it needs outside capital.

Frequently asked questions

It is current assets minus current liabilities: the short-term resources a company has to run its day-to-day operation without needing a fresh injection at every obligation that comes due.

Subtract current liabilities from current assets. Current assets include cash, receivables and inventory; current liabilities include suppliers, wages, taxes and debt due within a year.

On the asset side, cash in the bank, receivables from customers and inventory in stock. On the liability side, invoices owed to suppliers, wages and taxes due within the year. Working capital is the difference between the two.

Because it bills the subscription upfront and pays its costs over the following months. The customer funds the operation, so negative working capital becomes growth fuel rather than a sign of strain.

Because it represents money already received for a service the company will still deliver at high margin over time, with no cash outlay. It settles by shipping software, and signals annual contracts and future cash.

Related concepts

Cash flow

Cash flow is the difference between the money coming into a company and the money going out over a period. It splits into operating, investing and financing, and it is not profit: cash is what actually moves through the account. In SaaS, billing annual contracts upfront brings cash forward relative to recognized revenue.

Free cash flow

Free cash flow (FCF) is the cash left from operations after paying for capital investments (capex). It is the money truly available to pay down debt, reward investors or reinvest in growth. A SaaS that generates positive FCF funds itself and depends less on raising rounds.

Burn rate

Burn rate is the speed at which a company consumes its cash, almost always measured per month. Gross burn adds up all the money going out; net burn subtracts the revenue coming in and shows what actually drains the cash. It is the denominator of runway: the lower the burn, the more time a startup has before it needs new capital.