Break-even: what the break-even point is and how to calculate it

By Tiago Costa · Updated on July 9, 2026

Definition

Break-even is the level of sales at which revenue covers all costs and the result is zero.

- In units: fixed costs / unit contribution margin.

- Above it, each sale turns into profit; below it, into loss.

- Reaching it frees a startup from depending on external cash.

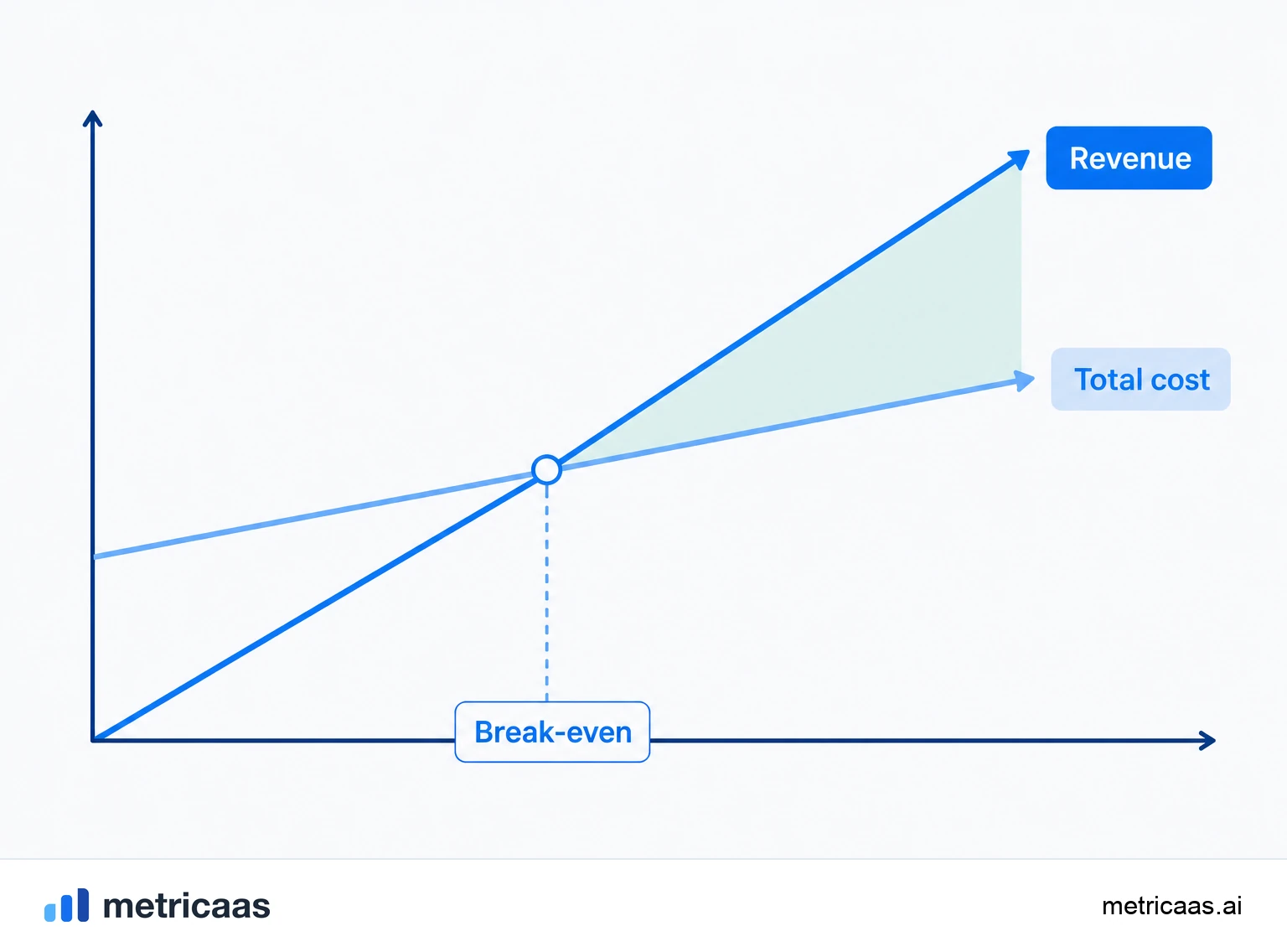

What break-even is

Break-even is the level of revenue or sales at which the company result is exactly zero: revenue covers every cost, with nothing left over and nothing missing. Below it, the operation runs at a loss; above it, each sale starts to generate profit.

It is simple to state and hard to reach. It answers a question every founder asks sooner or later: how much do I need to sell to stop burning money? As long as the answer sits above what the company sells today, it depends on external cash to exist.

How to calculate break-even

The most direct way is in units. Divide the period fixed costs by the unit contribution margin, that is, how much is left from each sale after variable costs.

- Break-even (units) = fixed costs / unit contribution margin.

- Fixed costs: rent, salaries, infrastructure, whatever does not change with volume.

- Unit contribution margin: price minus the variable cost of each sale.

Example: fixed costs of $50k per month and a contribution margin of $250 per subscription give a break-even of 200 subscriptions. Sell 200 and you break even; the 201st starts to turn a profit.

Break-even in units and in revenue

The same point can be read two ways. In units, it tells you how many sales you need to close. In revenue, it tells you what total billing zeroes the result.

- In units: fixed costs / unit contribution margin.

- In revenue: fixed costs / contribution margin ratio (the margin as a percentage of price).

Both versions describe the same place seen from different angles. In a SaaS, the revenue reading tends to be more useful, because it speaks directly to MRR and to sales targets; the units reading helps when every customer is worth roughly the same.

The profit zone above break-even

Above break-even the profit zone begins. There, the fixed costs are already covered, so almost the entire contribution margin of each new sale drops straight to the result. This is the operating leverage that makes growth so powerful once you pass break-even.

That is why break-even is a watershed and not just an accounting number. Below it, selling more deepens the loss if the margin is negative; above it, selling more multiplies profit. The distance between current revenue and break-even is the margin of safety: how far revenue can fall before the company goes back into the red.

Accounting and cash-flow break-even

There is a distinction that fools many people: accounting break-even is not the same as cash-flow break-even. The accounting one zeroes the result including expenses that do not leave your pocket in the month, such as depreciation. The cash one zeroes real money movement: it is the point where the company stops burning cash.

For a startup, the second is what matters in the end. As long as revenue does not cover cash outflows, there is a burn rate to finance, and runway counts the time until the money runs out. Reaching cash-flow break-even is the moment runway stops being a countdown.

Why reaching break-even frees a startup

Hitting break-even changes the nature of the business. The company stops depending on funding to survive and gets to choose when and why to raise. Investors such as Bessemer Venture Partners have talked for years about efficient growth, and break-even is the concrete proof that the operation sustains itself.

Getting there depends on healthy unit economics: a CAC that pays back in a reasonable time and a contribution margin that survives serving the customer. When each new customer contributes more than it costs to serve and acquire, break-even stops being a distant horizon and becomes a consequence of selling more.

Frequently asked questions

Break-even is the level of revenue or sales at which revenue covers exactly all costs and the result is zero. Below it there is a loss; above it, profit.

In units, divide fixed costs by the unit contribution margin. Fixed costs of $50k and a margin of $250 per sale give a break-even of 200 sales.

Break-even in units = fixed costs / unit contribution margin. The unit margin is price minus the variable cost of each sale.

Accounting break-even zeroes the result including non-cash expenses like depreciation. Cash-flow break-even zeroes real money, the point where the company stops burning cash.

Fixed costs are already covered, so almost all of each new sale contribution margin becomes profit. This is the profit zone, where growth leverages the result.

Because it is the moment the company stops depending on external cash to survive and gets to choose when to raise. It marks the shift to a business that sustains itself.

Related concepts

Contribution margin

Contribution margin is revenue minus variable costs, measured per unit or in total. It is what each sale leaves over to cover fixed costs and, after that, become profit. Unlike gross margin, which subtracts all of COGS, it isolates only what changes with volume, which is why it underpins break-even analysis and pricing decisions.

Burn rate

Burn rate is the speed at which a company consumes its cash, almost always measured per month. Gross burn adds up all the money going out; net burn subtracts the revenue coming in and shows what actually drains the cash. It is the denominator of runway: the lower the burn, the more time a startup has before it needs new capital.

Runway

Runway (cash runway) is how many months a company can keep operating on the cash it has, at its current burn rate. You calculate it by dividing available cash by the monthly net burn, and it sets the urgency to raise money or reach break-even. It is the financial breathing room that buys time to get the business right.