Contribution margin: what it is and how to calculate it

By Tiago Costa · Updated on July 9, 2026

Definition

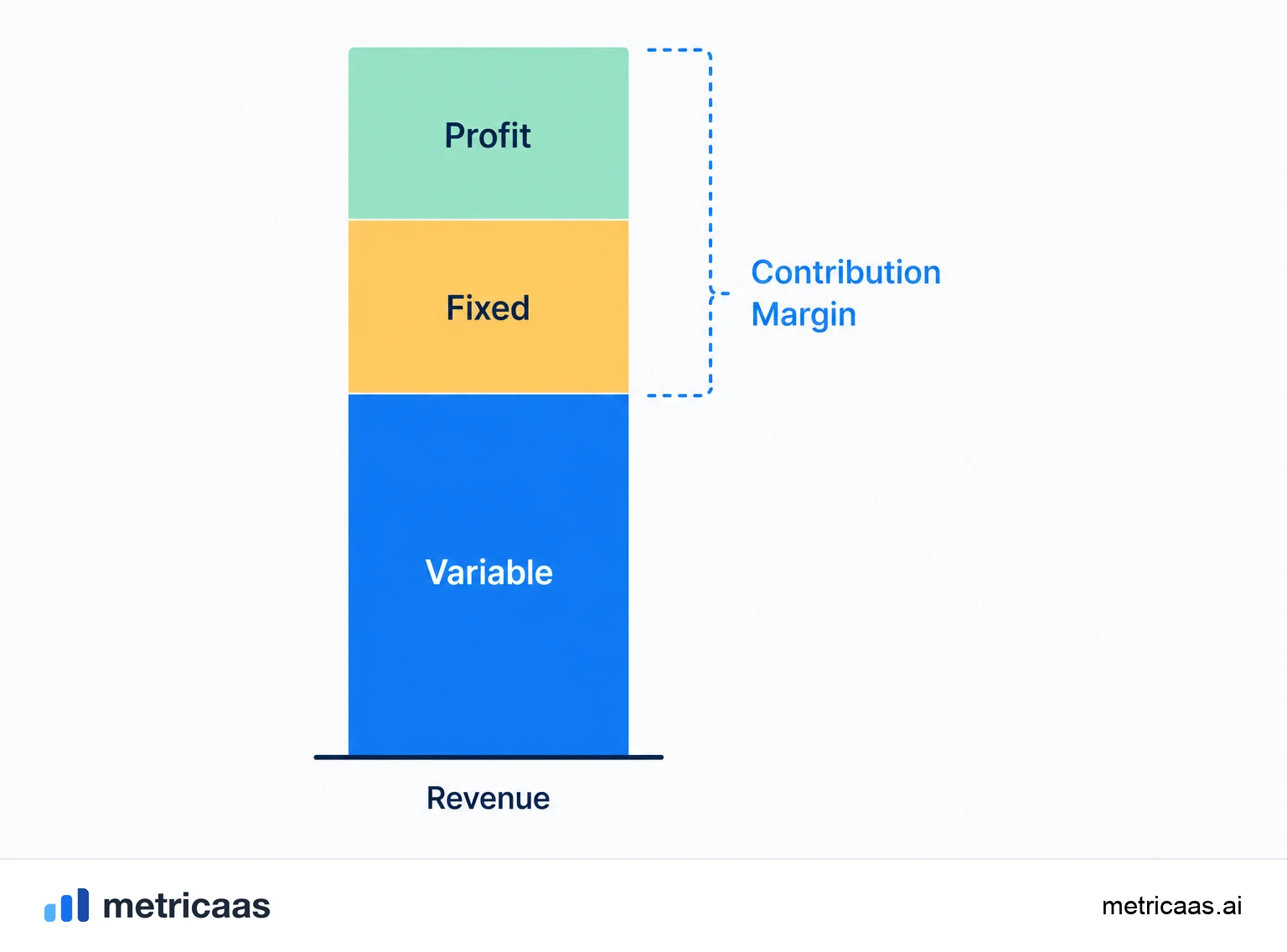

Contribution margin is revenue minus variable costs, per unit or in total: what each sale leaves over to cover fixed costs and turn into profit.

- Formula: revenue minus variable costs.

- Covers fixed costs first, the surplus is profit.

- Foundation of break-even analysis and pricing.

What contribution margin is

Contribution margin is how much a sale leaves over after paying the variable costs, the ones that only exist because the sale happened. The name comes from that: this amount contributes, first, to covering the fixed costs of the operation, and once the fixed costs are paid, every extra dollar of margin becomes profit.

It can be read two ways. In the per-unit version, it is the price of an item minus the variable cost of that item. In the total version, it is the period revenue minus all variable costs of the period. Both tell the same story: separating what varies with volume from what does not, so you can see clearly what each sale actually adds to cash.

How to calculate contribution margin

The formula is direct: revenue minus variable costs. As a percentage, you divide the margin by revenue to get the contribution margin ratio, useful for comparing products at different prices.

- Contribution margin = revenue - variable costs.

- Unit margin = price - variable cost per unit.

- Ratio (%) = contribution margin / revenue.

Only costs that grow with volume count as variable: raw materials, payment processing fees, sales commissions, per-order shipping and usage costs that rise with each customer. Example: a product sold at $100 with $40 of variable cost has a unit contribution margin of $60 and a 60% ratio. Fixed salaries, rent and company software stay out, because they do not change when you sell one more unit.

Contribution margin vs gross margin

Both measure profitability, but they cut the math at different points. Gross margin subtracts all of COGS, the cost of the products or services sold, which usually includes fixed portions such as part of the infrastructure or the production team. Contribution margin is more surgical: it subtracts only the variable costs, ignoring any fixed portion baked into COGS.

That is why contribution margin is usually higher than gross margin, and it answers a different question. Gross margin answers how profitable your product is after the full cost of delivering it. Contribution margin answers how much each extra sale injects to cover fixed costs. One looks at the structural health of the product, the other guides short-term volume and pricing decisions.

Contribution margin and break-even

This is where the metric shows its greatest practical value. The break-even point, the volume at which the company has neither profit nor loss, comes straight from contribution margin: just divide fixed costs by the unit contribution margin.

- Break-even (units) = fixed costs / unit contribution margin.

- Break-even (revenue) = fixed costs / contribution margin ratio.

Example: with $30k of fixed costs per month and a unit contribution margin of $60, break-even is 500 units per month. Sales above that become profit in proportion to the margin; below it, the operation burns cash. Raising the contribution margin, whether by lifting the price or trimming variable cost, lowers the break-even point and makes the business less fragile.

Using it in pricing and product mix

Contribution margin is the compass for two constant decisions: how much to charge and what to prioritize. On price, it shows the floor: selling below variable cost destroys cash on every sale, no matter how fast revenue grows. Above that floor, each price increase flows almost entirely into the margin.

On mix, it reorders priorities. A low-ticket product with a high contribution margin can be worth more than a high-ticket one with a thin margin, because it contributes more per dollar sold. Comparing products by margin ratio, rather than by gross revenue, avoids pushing volume that looks big but feeds fixed costs little. There is no universal number for a good margin: software businesses live with high contribution margins, while retail and manufacturing work with far smaller margins and make it up on volume.

Contribution margin in SaaS

In SaaS, variable costs per customer are low: hosting, payment processing and part of support. That is why the contribution margin per customer tends to be high, and it is what determines how long the company takes to recover CAC. The higher the margin per customer, the faster the acquisition cost pays back and the more room is left to reinvest.

The same logic climbs up to Operating margin: healthy contribution margins per customer, summed at scale, cover the fixed costs of team and structure and open room for profit. Efficiency frameworks popularized by firms such as Bessemer Venture Partners start from this base. And annual SaaS benchmark studies show high median gross margins, frequently above 70%, a sign of lean variable costs that sustain strong contribution margins.

Frequently asked questions

It is revenue minus variable costs, per unit or in total. It is what each sale leaves over to cover fixed costs and, after that, become profit.

By subtracting variable costs from revenue. As a percentage, you divide the margin by revenue. A product at $100 with $40 of variable cost has a $60 margin and a 60% ratio.

It is the selling price of a unit minus the variable cost of that unit. If the price is $100 and the variable cost is $40, the unit contribution margin is $60.

It depends on the sector. Software usually runs high contribution margins; retail and manufacturing run much lower ones and make it up on volume. What matters is that it covers fixed costs and leaves profit.

Gross margin subtracts all of COGS, including fixed portions. Contribution margin subtracts only variable costs. That is why contribution margin is usually higher and serves volume and pricing decisions.

For finding the break-even point, setting prices and prioritizing products. Break-even is fixed costs divided by the unit contribution margin.

Related concepts

Gross margin

Gross margin is the share of revenue left after the direct cost of delivering the service: (revenue minus COGS) divided by revenue, as a percentage. Pure SaaS usually runs between 70% and 85% or more, and that headroom is what sustains the model, feeds LTV and funds reinvestment in growth.

COGS

COGS (Cost of Goods Sold) is the direct cost of delivering a SaaS service: hosting and infrastructure, customer support, third-party fees and payment processing. It does not include sales, marketing or R&D, which are OpEx. It is the base of gross margin: revenue minus COGS equals gross profit.

CAC

CAC (Customer Acquisition Cost) is how much, on average, you spend to win a new customer. Add up everything invested in marketing and sales over a period and divide by the number of new customers who came in during that period. It is the metric that tells you whether your growth is economically healthy.