SAFE: what a Simple Agreement for Future Equity is and how it works

By Tiago Costa · Updated on July 9, 2026

Definition

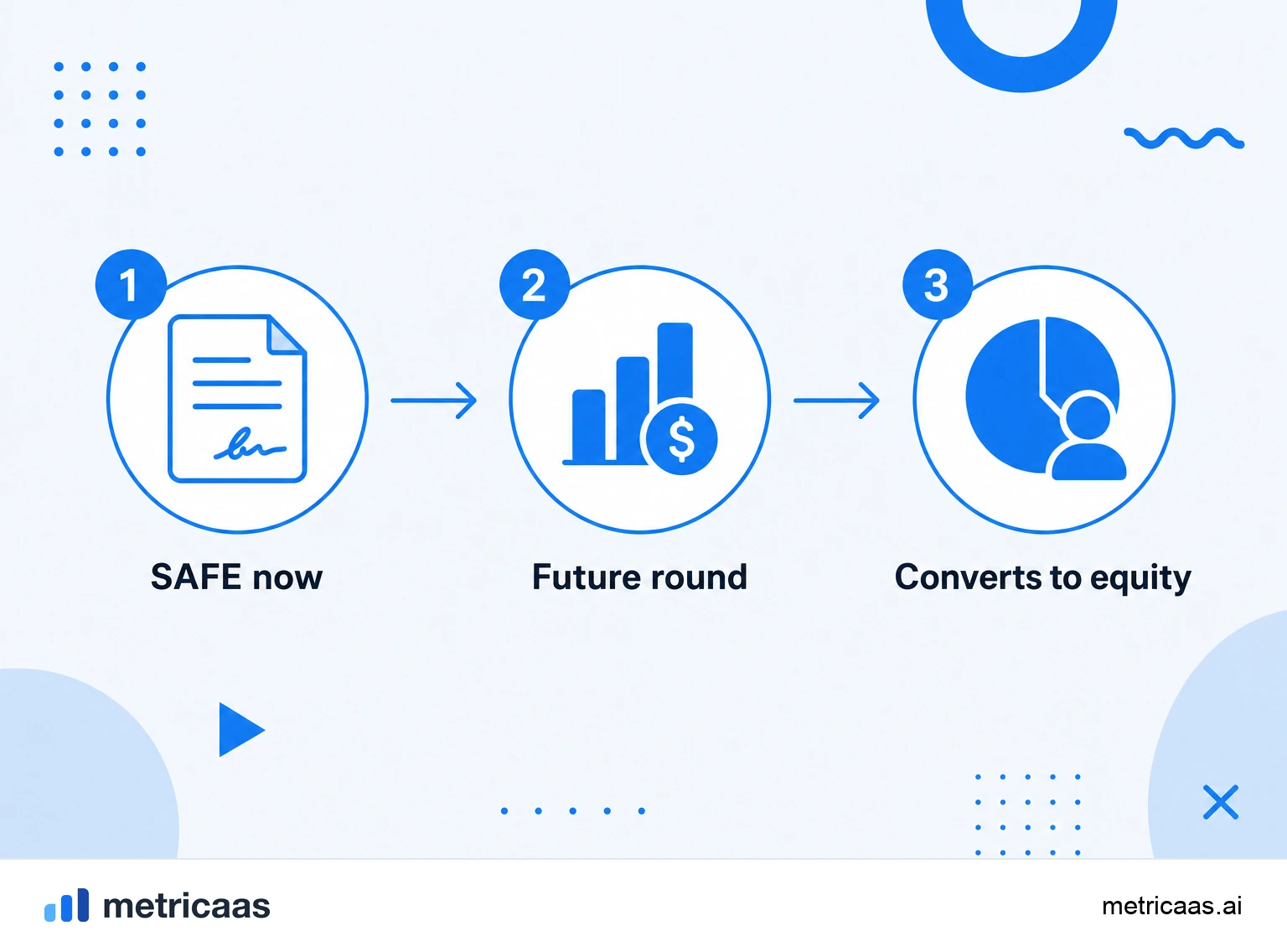

A SAFE (Simple Agreement for Future Equity) is the contract created by Y Combinator where an investor funds now and converts into equity at a future priced round.

- Defers the valuation decision to the next round.

- Rewards early risk with a valuation cap and/or a discount.

- It is not debt: no interest and no maturity.

What a SAFE is

The SAFE, short for Simple Agreement for Future Equity, is an early-stage investment contract created by Y Combinator in 2013. The idea is simple: the investor hands over the money today and, instead of receiving shares right away, gets the right to convert that investment into equity when the startup raises a priced round in the future. It pushes the hardest decision, how much the company is worth, to a moment when there will be better data to negotiate.

The format became a standard in the startup world because it cuts the paperwork and unlocks a fast check, valuable in a software market that keeps expanding: Gartner forecasts worldwide public cloud spending to reach $723 billion in 2025. Early-stage funds such as a16z and Y Combinator itself popularized the instrument precisely because it lets founders close seed rounds in days rather than months.

How a SAFE works

A SAFE has no price per share because, at signing, nobody yet knows what the startup is worth. The amount invested is recorded as a commitment to convert into equity. The conversion trigger is the next priced round (the so-called equity financing), when an investor comes in and negotiates a formal valuation and a price per share. At that point the SAFE turns into preferred shares.

- The investor signs the SAFE and transfers the capital.

- The money sits pending conversion, earning no interest.

- At the next priced round, the investment becomes shares based on the cap and/or the discount.

- From then on the investor formally appears on the company cap table.

Because it has no fixed price, a SAFE is far leaner than a traditional round, and it is common for most of the terms to come from a standard template rather than a long term sheet negotiated line by line.

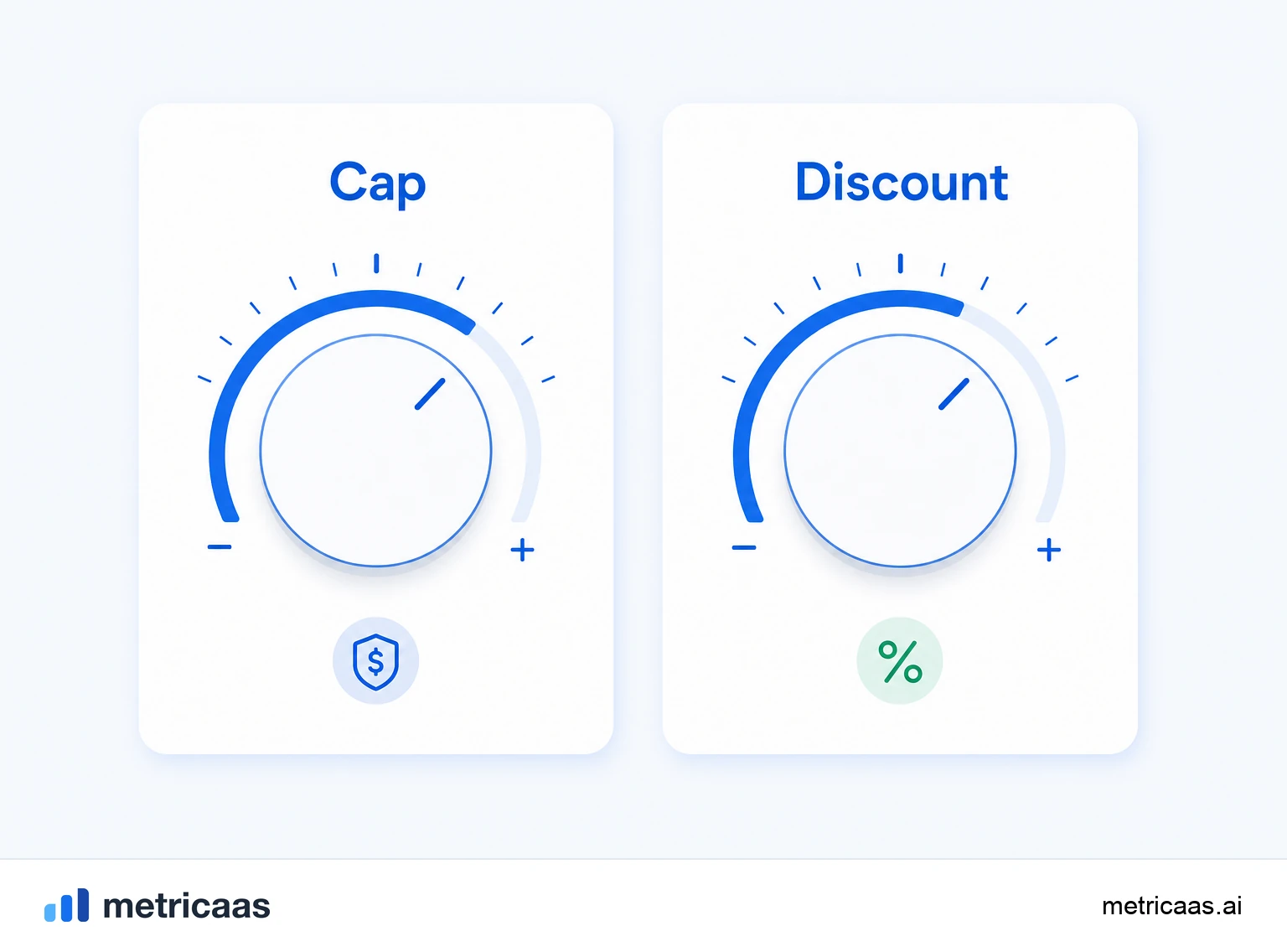

Valuation cap and discount

Since the SAFE investor comes in before everyone else and takes the most risk, the contract carries two mechanisms that let them buy shares cheaper than whoever arrives at the priced round. They can appear together or on their own, and when they are together, whichever is more favorable to the investor applies.

- Valuation cap: a ceiling on the valuation used for conversion. If the next round prices the company above that ceiling, the SAFE converts as if the valuation were the cap, giving the investor a bigger slice.

- Discount: a reduction on the round price per share, typically around 20%. Someone who came in through the SAFE pays, for example, 80% of the price paid by the new investors.

The cap protects an early investor when the company jumps in value, and the discount rewards the risk even when the valuation rises only a little. A SAFE can also carry neither cap nor discount and instead include a most favored nation clause, which grants the investor the best terms given to any future SAFE.

Pre-money and post-money SAFE

Y Combinator launched the original SAFE in 2013 with the cap referring to the pre-money valuation and, in 2018, published the post-money version, now the most widely used. The difference looks technical, but it changes who absorbs the dilution.

- Pre-money SAFE: the cap refers to the value of the company before the new money. Since you do not know how many other SAFEs and notes will convert alongside it, the investor final slice only becomes clear at the priced round, and everyone shares the dilution.

- Post-money SAFE: the cap already includes the total raised on SAFEs. That locks the investor percentage in a predictable way, calculated as the investment divided by the post-money cap. In exchange, the dilution from new SAFEs falls on the founders, not on those who already converted.

In practice, the post-money SAFE gives the investor clarity on the slice they will get, but it requires the founder to track the total raised closely, because each new SAFE dilutes their own position.

Stacked SAFEs and dilution

It is rare for a startup to raise a single SAFE. The common path is to stack several, with different caps and discounts, over months until the first priced round. That stacking is convenient, but it hides a trap: since they all convert at once in the same round, total dilution can surprise a founder who never added up the checks.

With post-money SAFEs the effect is even more direct. Each investor has their percentage locked, so each new SAFE signed does not dilute the earlier ones but the founders. Setting caps too low, or stacking investment beyond plan, can lead the founding team to hand over far more ownership than they expected when conversion finally happens. Modeling the conversion of every SAFE on the cap table before signing each new one is the best defense against that surprise.

A SAFE is not debt

A frequent confusion is treating a SAFE like a convertible note, but they are different in essence. A convertible note is a loan: it accrues interest and has a maturity date by which it must be repaid or converted. A SAFE is not debt, earns no interest and has no maturity, so it puts no deadline pressure and no default risk on the startup.

- SAFE: an instrument for future equity, with no interest and no term. It converts only if there is a priced round.

- Convertible note: debt with interest and maturity, which converts into equity or is repaid at the deadline.

That lightness is the main reason the SAFE became the standard for pre-seed and seed fundraising. It avoids the heavy negotiation of a full term sheet and puts no liability on the balance sheet, keeping the founder focused on growing until the round where the valuation will finally be set.

Frequently asked questions

It is the Simple Agreement for Future Equity, the contract created by Y Combinator where an investor funds now and converts that amount into equity at a future priced round, without setting a valuation at signing.

The investor hands over the money today and gets the right to convert into shares when the startup raises its next priced round. Conversion uses a valuation cap and/or a discount on the round price.

The cap is a valuation ceiling for conversion, giving more shares if the company ends up worth much more. The discount is a reduction on the round price per share, typically around 20%.

In pre-money the cap ignores other SAFEs and the slice is only clear at the round. In post-money the cap already includes the total raised on SAFEs, locking the investor percentage, with the dilution falling on the founders.

No. Unlike a convertible note, a SAFE has no interest and no maturity date. It is a commitment to convert into equity at a future round, without becoming a liability to repay.

Several SAFEs convert together in the same round, so total dilution can surprise you. With post-money SAFEs, each new investment dilutes the founders rather than the earlier investors, so you must add up every check.

Related concepts

Cap table

A cap table, or capitalization table, is the record of who owns what in a company: founders, investors and the employee option pool, always adding up to 100%. It lists shares, percentages and share classes, and it is rewritten at every funding round, when new investment dilutes the existing holders. It is the basis for negotiating valuation and the term sheet.

Valuation

Valuation is the estimate of what a company is worth at a given moment. In SaaS, the most common shortcut is a multiple on ARR, and that multiple rises or falls with growth, retention and efficiency, synthesized by the Rule of 40. Valuation also sets how much equity an investor gets for their check, separating pre-money (before the check) from post-money (after).

Dilution

Dilution is the drop in existing owners' percentage when the company issues new shares, typically in a funding round or when creating the option pool. You end up with a smaller slice of a hopefully bigger pie. Added up across rounds, dilution defines how much founders still hold at the end.