Down round: what it is, what it signals and when it makes sense

By Tiago Costa · Updated on July 9, 2026

Definition

A down round is a funding round raised at a lower valuation than the previous one.

- Signals that the old price did not hold, whether by market or performance.

- Dilutes shareholders more and can trigger anti-dilution provisions.

- Sometimes it is the rational way to avoid running out of cash.

What a down round is

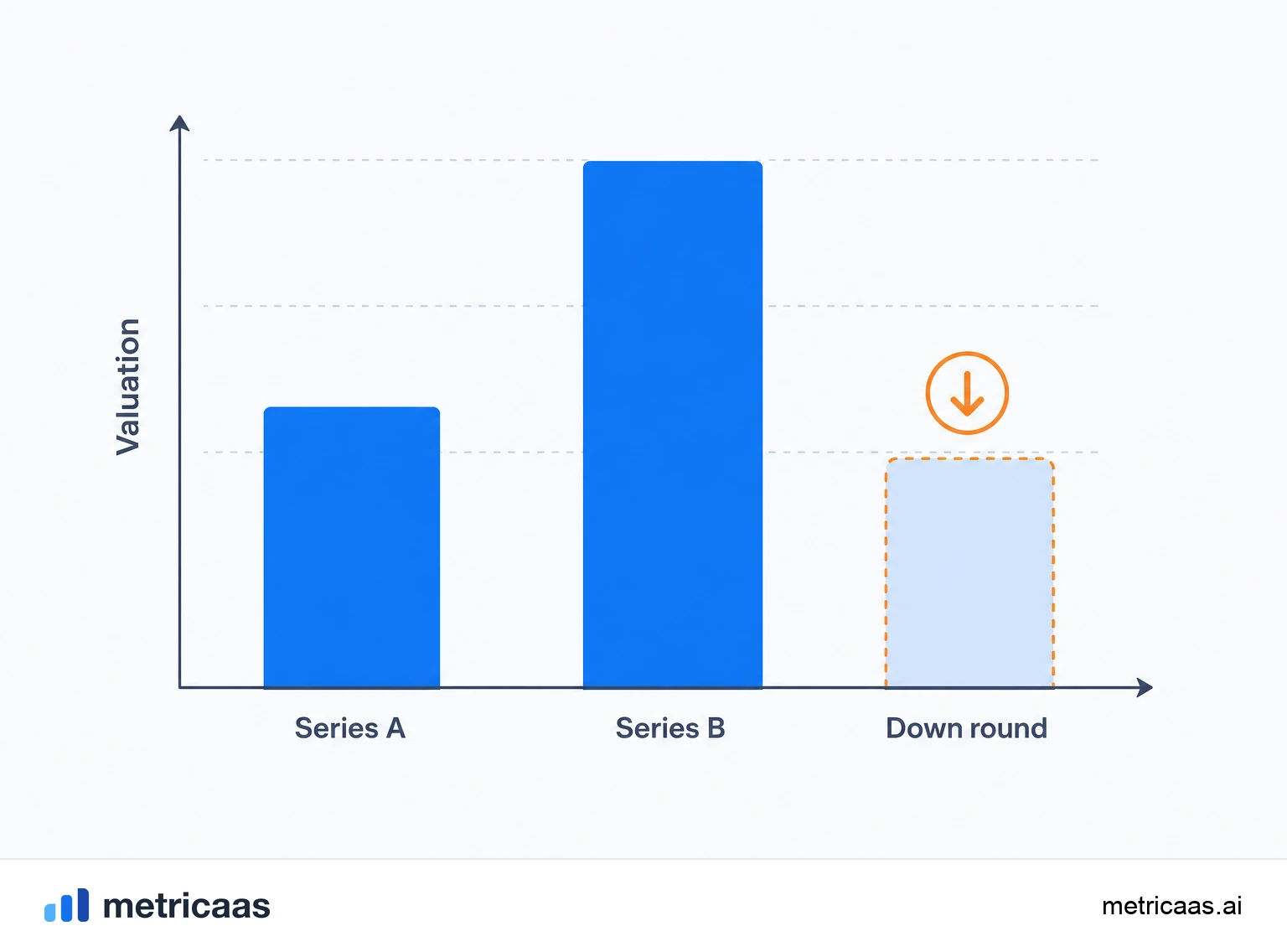

A down round is a funding round in which a company raises money at a lower valuation than its previous round. If a startup was worth $100 million at Series A and then raises a Series B at a $70 million valuation, that Series B is a down round.

The opposite is an up round, at a higher valuation, and the middle ground is a flat round, where the value stays the same. What defines the category is not the size of the check but the price per share: if it falls versus the last priced round, it is a down round, even if the company is raising more money in absolute terms.

What a down round signals

A down round almost never happens by accident. It signals that the market or the company performance did not hold up the price agreed before. It can be internal, such as growth below plan, high churn or cash burning faster than revenue, or external, such as a shift in investor appetite and a broad compression of multiples across the sector.

It is worth separating the two cases. When the valuation drops because the whole sector repriced, the down round says little about the quality of the business; plenty of good companies went through it during tighter credit cycles. When it drops because the company itself did not deliver, the signal is harsher and usually comes with a revised plan. Bessemer often points out that valuations set in hot markets rarely hold when the cycle turns, and that correcting the price is not the same as breaking the thesis.

Dilution and anti-dilution provisions

The most concrete effect of a down round is dilution. Because the price per share is lower, more shares must be issued to raise the same amount, and the stake of founders and early investors shrinks more than it would in an up round. On top of that, many contracts from earlier rounds carry anti-dilution provisions that trigger precisely when the price falls.

- Full-ratchet: the most aggressive. It reprices the old investor preferred shares as if they had come in at the new, lower price, ignoring how much they bought. It protects the investor heavily and dilutes founders hard.

- Weighted-average: the most common. It adjusts the conversion price taking into account both the price and the volume of the new issuance, which softens the blow. It comes in broad-based and narrow-based versions, depending on the share base considered.

These provisions genuinely reshape the cap table. It is worth simulating the effect on the cap table before closing, because a full-ratchet can transfer a surprising slice of control to whoever invested in the previous round.

When a down round is the rational choice

Accepting a lower valuation hurts, but sometimes it is the most rational decision on the table. If the runway is running out and the only alternatives are shutting down, a fire sale at any price, or a down round that keeps the company alive and funded for another 18 or 24 months, the down round is usually the best of the bad paths.

The logic is simple: a proud valuation does not make payroll. Cash in the bank buys time to fix what stalled, prove growth again and raise later on better terms. Many businesses that are solid today went through a down round along the way, and no one remembers, because what stuck was the recovery, not the price of one specific round.

Recaps and structured rounds

When the gap between the old valuation and the new one is too wide, the round sometimes stops being a simple down round and becomes a recapitalization, or recap. In a recap, the capital structure is redesigned: there may be a forced conversion of preferred into common, a reset of liquidation preferences, or even a pay-to-play, where an investor who does not join the new round loses part of their rights.

There are also so-called structured rounds, where the headline valuation stays high but the investor gets heavy protections: a two or three times liquidation preference, guaranteed dividends, seniority. It is a disguised down round, because the nominal price misleads and the real economic value for founders has fallen. Reading the full structure, not just the valuation number, is what reveals whether the round is good or only looks good.

How a stretched valuation and short runway lead to a down round

The classic path to a down round has two ingredients that combine. The first is a stretched prior valuation, raised at a peak of optimism, too high for the real stage of the business. The second is a runway that tightens before the company has grown enough to justify that price.

When the two meet, the math does not work: the company needs cash but cannot defend the old valuation against its current metrics. The antidote is not to overprice the good rounds, to measure growth and retention honestly, and to watch the runway with a margin, raising before cash gets short. A round price is a promise; if the promise was too big, the market collects the difference in the next round.

Frequently asked questions

It is a funding round in which a company raises at a lower valuation than its previous round. What defines it is the price per share falling, even if the amount raised is larger.

No. When the whole sector repriced, it says little about the business. And keeping the company funded for longer is often worth more than defending an old valuation.

They are protections that reprice the old investor shares when a round is raised at a lower price. The main ones are full-ratchet, the most aggressive, and weighted-average, the most common.

Full-ratchet reprices as if the investor had come in at the new lower price, diluting founders hard. Weighted-average considers the price and volume of the new issuance and softens the effect.

No. In a flat round the valuation stays the same; in a down round it falls. An up round is the opposite, at a higher valuation than the previous round.

When the runway is short and the alternative is shutting down or a rushed sale. Cash in the bank buys time to fix what stalled and raise again on better terms.

Related concepts

Valuation

Valuation is the estimate of what a company is worth at a given moment. In SaaS, the most common shortcut is a multiple on ARR, and that multiple rises or falls with growth, retention and efficiency, synthesized by the Rule of 40. Valuation also sets how much equity an investor gets for their check, separating pre-money (before the check) from post-money (after).

Dilution

Dilution is the drop in existing owners' percentage when the company issues new shares, typically in a funding round or when creating the option pool. You end up with a smaller slice of a hopefully bigger pie. Added up across rounds, dilution defines how much founders still hold at the end.

Cap table

A cap table, or capitalization table, is the record of who owns what in a company: founders, investors and the employee option pool, always adding up to 100%. It lists shares, percentages and share classes, and it is rewritten at every funding round, when new investment dilutes the existing holders. It is the basis for negotiating valuation and the term sheet.