Gross vs net revenue: what they are, the difference and how to calculate

By Tiago Costa · Updated on July 9, 2026

Definition

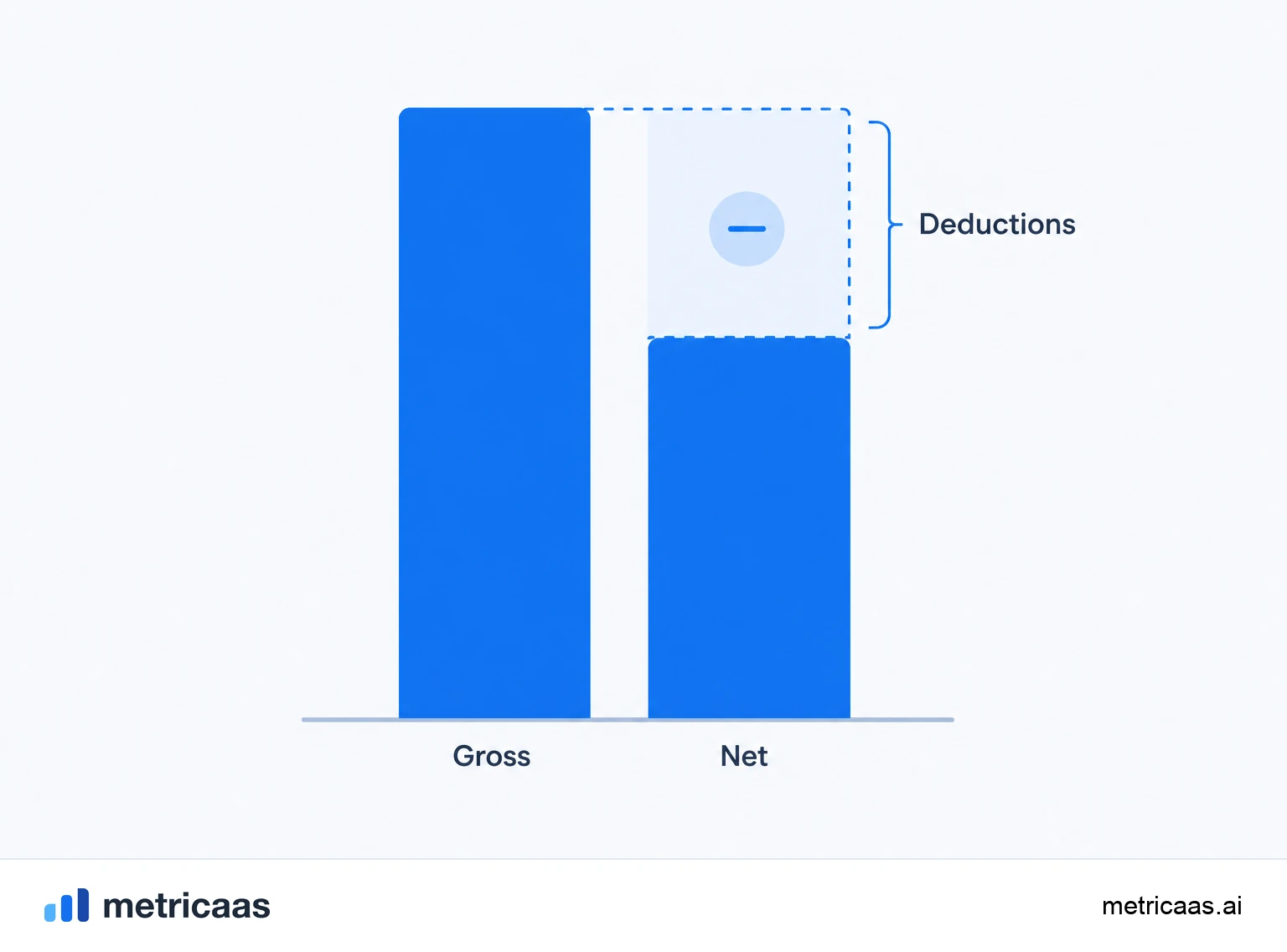

Gross revenue is the total billed before deductions; net revenue is what remains after discounts, refunds, gateway fees and taxes.

- Gross shows the size of billing; net shows the real revenue.

- Net = gross minus discounts, refunds, fees and taxes.

- The difference matters for margin and revenue recognition.

What gross and net revenue are

Gross revenue is the total billed in a period, before any deduction. It is the full number, the sum of every charge issued. Net revenue is what remains of that total after removing discounts, refunds, processing fees and taxes, in other words, what the company actually keeps.

The distinction is easy to state and easy to blur in practice. Gross revenue shows the size of billing; net revenue shows the real revenue that funds the operation. A business can have high gross revenue and much lower net revenue if it runs on heavy discounts, refunds or taxes.

How to calculate net revenue

Net revenue starts from gross and subtracts everything that does not stay with the company. The formula is direct:

- Net revenue = gross revenue - discounts - refunds and chargebacks - gateway fees - taxes.

- Start from the total billed in the period (gross revenue).

- Subtract each deduction in the order it reduces the amount that actually reaches cash.

Example: a company bills $100k in a month (gross). If it grants $8k in discounts, returns $3k in refunds, pays $3k in payment fees and collects $12k in taxes, net revenue is $74k. That figure, not the gross one, reflects the money available to cover costs and generate margin.

What counts as a deduction from revenue

Not every deduction carries the same weight, and understanding each one keeps you from measuring revenue too optimistically. The main ones are:

- Discounts and allowances: coupons, promotions and commercial concessions that lower the price charged.

- Refunds and chargebacks: money returned or disputed that gives the customer back part or all of an amount already billed.

- Gateway and processing fees: the slice the payment provider keeps on each transaction.

- Taxes: sales taxes the company merely collects and passes on, never keeping them.

Taxes deserve special attention. Because the company only collects and remits them, they almost never belong in recognized revenue. Gateway fees and refunds, in turn, are often underestimated, yet they quietly erode margin when transaction volume is high.

Why the difference matters: margin and recognition

Separating gross from net is not accounting fussiness, it is what lets you read margin honestly. Margin is calculated on net revenue, because net is the real money; using gross inflates the metrics and hides how much each sale actually leaves behind.

There is also revenue recognition. Standards such as IFRS 15 and ASC 606 govern when and at what amount revenue enters the books, including the classic principal versus agent question: a party that merely intermediates a sale recognizes only its commission (net), not the full amount passing through its hands (gross). Reporting gross when net is correct is one of the most common findings in audit.

Gross and net revenue in a subscription SaaS

In a SaaS, recurring revenue amplifies the gap between gross and net, because every distortion repeats each month. MRR should reflect real recurring revenue, already clear of promotional discounts and refunds, not the full face value of the invoices issued. Counting gross as if it were net overstates growth month after month.

Churn and refunds pull net revenue down further: cancellations, refunds and chargebacks reduce what the company actually keeps. This care matters in a large market, worldwide public cloud spending is set to reach $723 billion in 2025 according to Gartner, and at that scale even small percentage gaps between gross and net turn into meaningful figures.

Common mistakes when separating gross from net

The most frequent slips come from mixing the two bases or comparing numbers that are not comparable:

- Reporting gross and calling it net: inflates revenue and margin, and one day the number will not reconcile with cash.

- Forgetting payment fees: they look small per transaction but add up over time.

- Ignoring refunds and chargebacks: booking the sale and never reversing the returned amount overstates real revenue.

- Confusing net revenue with profit: net revenue has not yet subtracted the cost of running the business; profit is what is left after that.

Net revenue answers how much the company really earns from its sales; profit answers how much is left after all costs. They are different questions, and swapping them leads to wrong decisions about price, margin and growth.

Frequently asked questions

It is what remains of gross revenue after removing discounts, refunds, gateway fees and taxes. It represents the money the company actually keeps.

Gross is the total billed before deductions; net is that total already free of discounts, refunds, fees and taxes. Gross shows the size, net shows the real revenue.

Start from gross revenue and subtract discounts, refunds and chargebacks, payment fees and taxes. What is left is net revenue.

After. Net revenue already excludes sales taxes, which the company only collects and remits, so they rarely form part of recognized revenue.

No. Net revenue has not yet subtracted the cost of running the business. Profit is what remains after all those costs.

Because revenue is recurring: counting gross as net in MRR overstates growth every month and distorts margin and recognition.

Related concepts

MRR

MRR (Monthly Recurring Revenue) is the monthly recurring revenue of a SaaS: the sum of all active subscriptions normalized to a month. It is the core metric of a subscription business because it shows, predictably, how much the company earns on a recurring basis each month, without counting one-off charges.

Churn

Churn is the loss of customers or revenue in a period. In a SaaS, it measures how many customers cancel (customer churn) or how much recurring revenue disappears (revenue churn). It is the metric that reveals whether growth is sustainable: the higher the churn, the more new sales you need just to avoid shrinking.

ARR

ARR (Annual Recurring Revenue) is the annual recurring revenue of a SaaS: MRR multiplied by 12. It represents how much the company earns on a recurring basis over a year, counting only active subscriptions, with no one-off charges. It is the metric of choice for companies selling annual contracts and the standard language of investors.