Chargeback: what it is, how it works and how to reduce it

By Tiago Costa · Updated on July 9, 2026

Definition

A chargeback is the forced reversal of a charge: the customer disputes the purchase with their bank and the amount is reversed, undoing the sale.

- Reverses the sale and triggers a fee charged by the acquirer.

- It is a form of involuntary churn and, often, of fraud.

- A clear billing descriptor and renewal reminders reduce how often it happens.

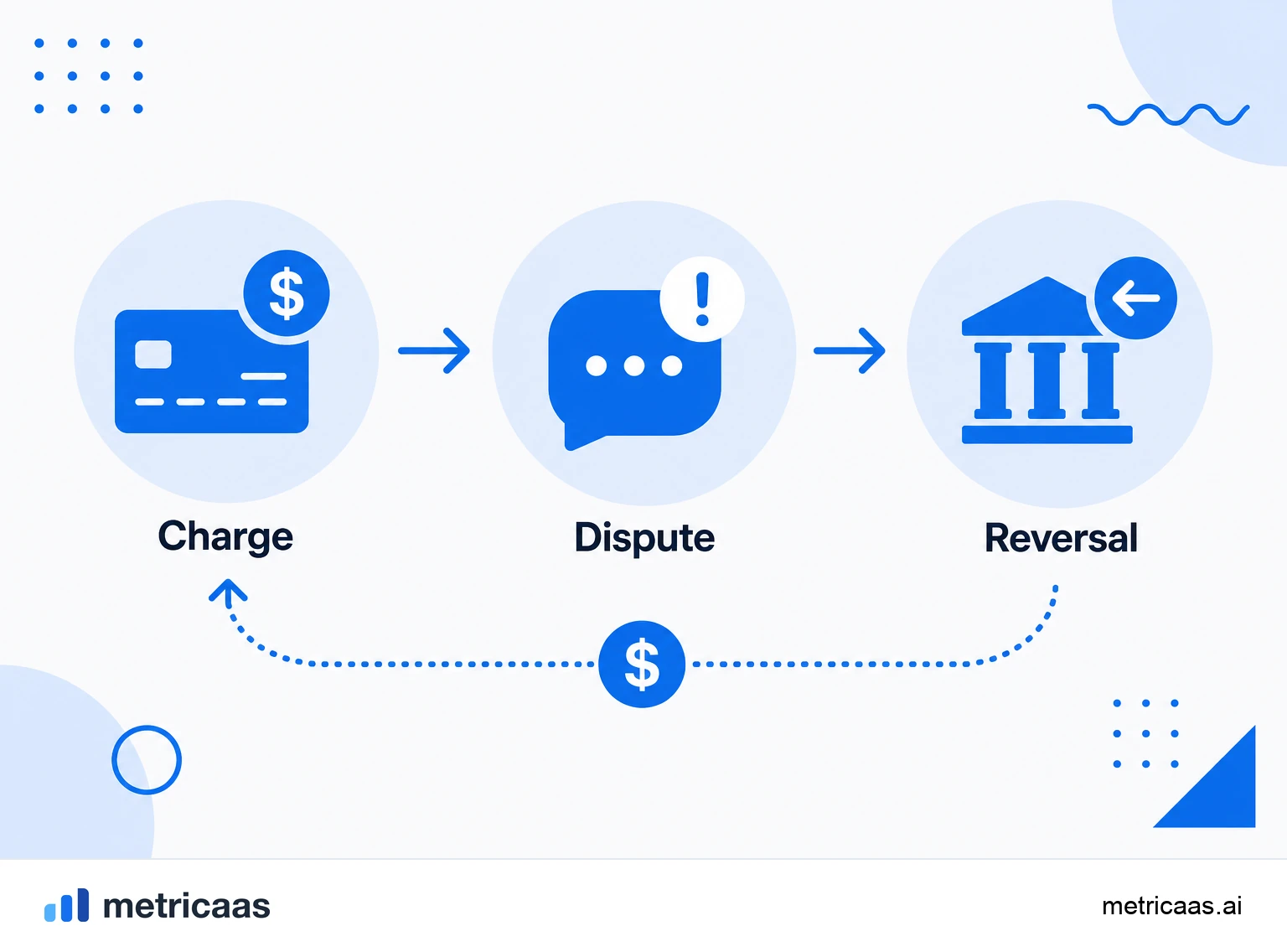

What a chargeback is

A chargeback happens when the cardholder disputes a charge directly with their issuing bank, and the bank reverses the amount by force, pulling the money out of the business and returning it to the customer. A sale that looked complete is undone, and it happens outside the merchant: the issuer decides, following the card network rules.

The mechanism was created to protect consumers against unrecognized charges, undelivered goods or card fraud. In a SaaS, it tends to show up in renewals the customer forgot about, in charges whose name on the statement they do not recognize, or in subscriptions they chose to dispute at the bank instead of cancelling. The payment usually flows through a payment gateway, but the dispute itself runs between the customer bank and the acquirer.

Chargeback, refund and reversal: the differences

The three terms sound like synonyms but describe different paths. In a refund, the business itself returns the money to the customer, by choice, inside its own system. In a chargeback, the customer bank forces the return, without going through your approval and often without warning.

- Refund: you return the amount on your own initiative, with no dispute fee.

- Chargeback: the bank reverses the charge by force, and the acquirer charges the business a fee.

The practical difference is large: a refund is your decision and does not count against you in the card network ratios; a chargeback is a formal dispute that enters your dispute rate and can trigger penalties. That is why resolving the customer request before they call the bank is almost always cheaper.

How the chargeback process works

The cycle starts when the customer disputes the charge with the issuing bank. The bank opens the dispute, provisionally credits the customer and notifies the acquirer, which passes the challenge on to the business along with a motive, the so-called reason code. From there, the merchant can accept the loss or present a defense.

That defense is representment: the business gathers evidence that the charge was legitimate, such as product usage logs, acceptance of the terms, delivery proof and access history, and sends it to the issuer, which has the final say. Winning the dispute recovers the revenue, but the process eats time and does not always reverse the fee already charged. That is why prevention pays off more than defense.

Who bears the cost

In the vast majority of cases, the business bears the cost, not the bank or the card network. When a chargeback is finalized, the merchant loses the revenue from the sale, also loses the product or service already delivered, and still pays a chargeback fee to the acquirer, which is usually charged even when the dispute is later won.

There is a cost more dangerous than the sum of those losses: the chargeback ratio. Card networks track the proportion of disputes to sales and, when it crosses the thresholds of their monitoring programs, the business can fall into regimes of fines, held reserves and, ultimately, the loss of its ability to process cards. Keeping that ratio low is a matter of operational survival, not just margin.

Chargeback as involuntary churn and fraud

From a metrics standpoint, a chargeback is a form of involuntary churn: the customer leaves the base without a clear cancellation decision, through a payment friction. They should have kept paying, but the subscription is interrupted by a dispute, and the effect on churn and recurring revenue is the same as any other loss.

Part of chargebacks is pure fraud, with stolen cards. Another part, very common in subscriptions, is so-called friendly fraud: the customer recognizes the purchase but disputes it anyway, out of forgetfulness or because it feels easier than asking to cancel. Because this leak hits retention, it drags down metrics the market watches closely: the private SaaS survey by KeyBanc Capital Markets shows net revenue retention above 100%, and every chargeback works against that number.

How to prevent and reduce chargebacks

Preventing is cheaper and more effective than disputing. The first front is making the charge recognizable: a clear billing descriptor, with a name the customer associates with the product, avoids much of the "I do not recognize this" disputes. The second is communicating: renewal reminders before the charge, email receipts and an easy way to cancel remove the customer incentive to go to the bank.

- Use a clear, recognizable billing descriptor.

- Send renewal reminders and receipts before charging.

- Offer easy cancellation and refunds, before it becomes a dispute.

- Fight payment failure at the source, with retries and card updates.

- Monitor your chargeback ratio and the most frequent reasons.

Because a chargeback is a slice of retention, cutting it protects the very result that sustains growth. Market references such as those compiled by SaaS Capital show that high retention rates separate the best SaaS from the rest, and containing involuntary churn is one of the most direct levers to get there.

Frequently asked questions

It is the forced reversal of a charge: the customer disputes the purchase with their issuing bank and the amount is reversed by force, undoing the sale, without going through the business approval.

In a refund, the business returns the money by choice, with no dispute fee. In a chargeback, the customer bank forces the return, charges the business a fee and counts against its dispute ratio.

Almost always the business. It loses the revenue, loses the product or service already delivered and still pays a fee to the acquirer, which is often charged even when the dispute is later won.

The customer disputes with the bank, which opens the dispute and notifies the acquirer. The business can accept the loss or present a defense (representment) with evidence that the charge was legitimate, and the issuer decides.

No. A refund is a return you choose to make, with no dispute fee. A chargeback is a return imposed by the customer bank, with a fee and an impact on your ratio with the card networks.

Use a clear billing descriptor, send renewal reminders and receipts before charging, offer easy cancellation, fight payment failure at the source and monitor your dispute ratio.

Related concepts

Involuntary churn

Involuntary churn is the cancellation of a subscription caused by a payment failure, such as a declined, expired or maxed-out card, rather than a customer decision. It usually accounts for a meaningful slice of total churn and is highly recoverable with dunning, that is, payment retries and requests to update the card.

Payment gateway

A payment gateway is the service that sits between the customer and the bank (or acquirer) and processes each charge: it authorizes the card, tokenizes the data so it never lives in your system, and retries payments that fail. In subscription SaaS, a good gateway with smart retries recovers declined charges and reduces involuntary churn. Stripe and Asaas are examples.

Churn

Churn is the loss of customers or revenue in a period. In a SaaS, it measures how many customers cancel (customer churn) or how much recurring revenue disappears (revenue churn). It is the metric that reveals whether growth is sustainable: the higher the churn, the more new sales you need just to avoid shrinking.